7 minute read

Given the current COVID-19 pandemic, it may seem like an odd time to talk about wealth transfer planning. Nevertheless, for those with large enough estates to be concerned about estate taxes, the pandemic, along with the current beneficial U.S. transfer tax laws, have created a favorable estate tax planning environment. This environment enhances the benefits of many estate planning strategies, which could translate into substantial estate and gift tax savings. Time to act is of the essence, though, since it is difficult to predict how long these favorable conditions will remain in place.

The three main reasons for the current favorable estate tax planning environment include:

- Substantial lifetime estate and gift tax exemption, which is more than double what the previous highest exemption amount was.

- Low interest rates which enhance the benefits for certain wealth transfer strategies.

- Possible lower valuations for closely held businesses and other assets.

Reason #1: The beneficial (but likely temporary) estate and gift tax laws

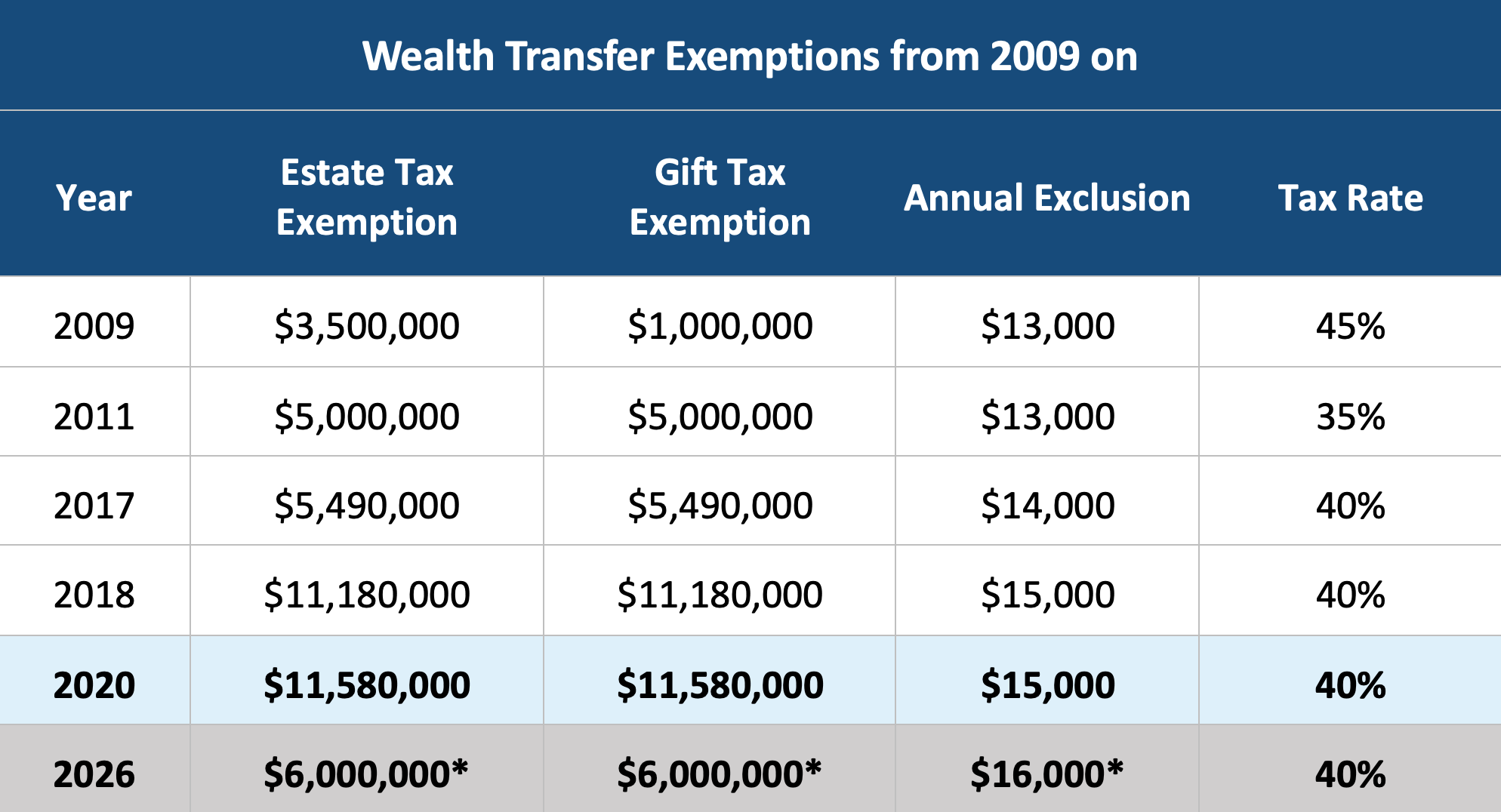

The above chart reflects the lifetime estate and gift tax exemption from 2009 to the present amounts. As a result of the 2017 Tax Cuts and Jobs Act (TCJA) the estate and gift tax exemption amounts in 2017 were doubled. This substantial increase is beneficial because the higher the exemption amounts, the more likely an individual or married couple will not have to pay estate or gift taxes. If one makes a gift while he or she is alive or a bequest at death, gift or estate tax will only due if the total amount of lifetime gifts and/or bequests exceed the exemption amount. Under the current law, and assuming you are married, the total exemption that would generally be available for US citizens in 2020 is $23,160,000 ($11. 58 million times two), which is about $12 million more than what it was in 2017.

The only issue is that the current exemption amount is temporary. Under the TCJA, the exemption is set to expire at the end of 2025 when it will return to an inflation adjusted $5 million amount. Also, since 2020 is an election year, the exemption could be reduced well before 2025 depending on the election results. Given how significantly it was increased, there is a strong likelihood that it would be decreased if there is a political change. The open question is how much it will be reduced.

The only way for a high net worth individual to utilize this higher exemption amount is to make taxable gifts (unless of course they pass away). One advantage of making taxable gifts is once a gift is made, and if it is properly planned, any subsequent growth on the amount gifted is excluded from the estate. As mentioned, an individual can currently give $11.58 million with no gift taxes versus the projected inflated $6 million amount which will be available in 2026 (again, this amount could change before 2025 if the law is changed). Even though most will not be able to make large enough gifts to take advantage of the higher exemption, those who can could save substantial gift and/or estate taxes.

Let’s illustrate this impact with an example. John, single, has a sizable net worth, so he decides to give $11.58 million of assets this year (2020) to an irrevocable trust for the benefit of his children and because this equals his available gift exemption, he does not have to pay any gift taxes on the transfer. A consequence of this approach is that he likely has used up all of his exemption so there may not be any of it left when he dies. He then dies in 2026, and assuming there is no change made to estate and gift tax law, the exemption amount at that time is $6 million. By making this gift in 2020, he was able to remove $5,580,000 out of his estate ($11,580,000 - $6,000,000), which he could not have done in 2026. This results in a tax saving of close to $2.2 million. The savings could even be greater if the value of the initial gift has grown in value, since any related appreciation will also be out of the estate and not

These strategies can be used by those who may not be able to make gifts large enough to take advantage of the current gift exemption, but who may still have a sizable estate tax issue (especially if the exemption is reduced). For example, Jack and Jill (married), are both in their early 60’s and are in good health. They have a total net worth of $20 million. They have two children and several grandchildren, and would like to bequest their wealth to them with minimal transfer taxes. In the unlikely event of their deaths before 2025, there will be no estate tax due since their net worth is under the available combined exemption amount. The more likely scenario is they will survive until after 2025, and at that time, unless the law is changed, there will be substantial estate taxes owed. Given this situation, Jack and Jill may want to consider taking steps now to minimize the impact of future estate taxes, especially given the other factors which make this current time a favorable environment for estate tax planning.

Reason #2: Low interest rates

There are various rates used in estate planning calculations and they are currently at or near record lows. These low rates provide significant leverage opportunities for estate planning purposes. These low rates include the Applicable Federal Rates (AFR), which are rates that are published monthly by the IRS and represent the minimum interest rate that must be charged for loans between family members. There are three different AFRs, short-term (for loans with term of 3 years or less), mid-term (loans with terms 3 to 9 years), and long-term (loans with terms more than 9 years).

The mid-term AFR is currently at a very low 0.45% (it was at 0.43% in June and was 1.93% as recently as March 2020). The leverage opportunity is illustrated by the following example. Assume that a mother decides to loan $1 million to her son. The loan is set up to require annual interest only payments until the loan matures in 9 years. Since the loan will be issued in July, the interest rate on the loan is 0.45%. As a result, at the end of the first year, the son will have to pay $4,500 in interest. If he reinvests the loan proceeds and obtains a 6% growth rate, he will be able to keep the growth which exceeds the interest paid or $55,500 since this resulted from a valid loan transaction this excess amount is not considered a taxable gift. This example illustrates the substantial leverage opportunity available due to the low AFRs. Since many estate planning strategies utilize loan transactions, these strategies (such as a Note Sale to an Intentionally Defective Grantor Trust) are also benefited by the current low rates.

The AFRs are also used to calculate the IRC Section 7520 rate (7520 rate). This rate is used with certain transfer strategies such as a Grantor Retained Annuity Trust (GRAT). Certain strategies like GRATs are advantageous in a low interest rate environment. Since the 7520 rate is determine by using the mid-term AFR, the current 7520 rates for June and July is at an all-time low of 0.60%. This favorable GRAT environment, coupled with the fact that asset values may be down due to COVID-19, creates an opportunity to be able transfer substantial wealth while minimizing and possibly eliminating gift taxes.

Reason #3: Favorable valuations due to COVID-19

The amount of gift or estate taxes owed is directly correlated to the value of the assets being transferred. The higher the value of the assets transferred, the higher the taxes, while the lower the value, the lower the taxes. Due to COVID-19, asset values may be depressed, and could afford a gifting opportunity. This is particularly true if this lower value is primarily caused by the pandemic and is considered a temporary drop in value.

For those who own a business, the economic disruption and business risk caused by the pandemic could allow for a lower value for the business. This may be especially true for industries where there are likely to be shifts in demand, loss of customers, gloomy outlook, disruptions in supply chain, and other possible disruptions cause by COVID-19. If a closely held business makes up a significant portion of an individual’s estate, it may be an opportune time for the business owner to transfer a portion or all of the business to family members because of the favorable lower valuation that they may be able to obtain.

Summary

Given the current uncertainty caused by COVID-19 it may indeed seem like a strange time to consider transferring wealth to the family. Nevertheless, it is this uncertainty which has resulted in a favorable estate planning environment caused by low interest rates and depressed asset values. These factors, coupled with a favorable U.S. transfer tax law, makes it a great time to transfer wealth.