6 minute read

Smart insight and clear visuals that matter – what we’re watching now and how intention and conviction shape our portfolios.

Stock Market

SpaceX was priced last night at an initial $135 per share and opened at $150 per share at approximately 8:50am PST. (Source: Reuters; TechCrunch, June 12, 2026)

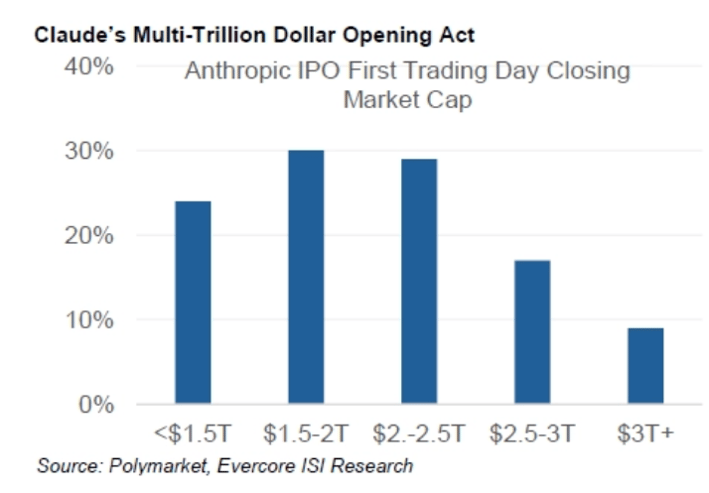

The WSJ ran a story this week that could impact the fee pool for two mega-cap companies widely reported to be next in line, Anthropic and OpenAI. The piece reads somewhat like a shot across the bow, potentially signaling positioning from bankers aligned with OpenAI as Anthropic continues to share gains. While price cuts were always expected in this market, it was generally assumed it would come later as capital intensity waned.

IPO: Anthropic and OpenAI

Over the next few months, public equities are expected to absorb a massive wave of AI-driven capital formation from the “AI IPO Wave.” Anthropic has reportedly filed confidentially for a fall IPO (Source: Bloomberg, June 1, 2026), with early market estimates indicating an expected initial valuation of roughly $2.25 trillion. Prediction markets assign a 7% chance that Anthropic scales to a $5 trillion valuation by the close of 2026.

As OpenAI also moves toward a fall public offering, investors should anticipate major shifts in capital allocation as these mega-cap alternatives hit the market.

Small Cap

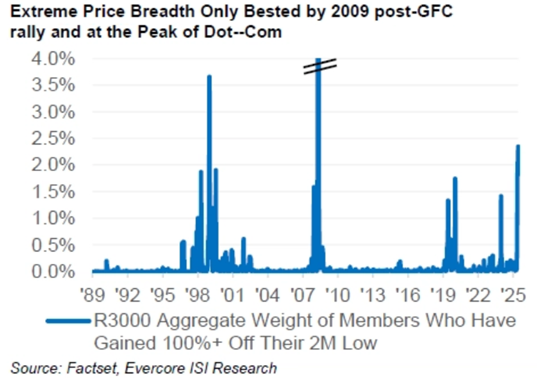

Over the past two months, 86 stocks in the Russell 3000 — representing just ~2.5% of index weight — have doubled in value, an intensity of momentum not seen since the immediate post-GFC rebound in 2009. This kind of outsized gain concentrated in a narrow subset of names signals a non‑normal regime: returns are being driven less by broad-based fundamentals and more by scarcity, positioning, and reflexive flows. The result is a structurally fragile setup — one where leadership is thin and vulnerable, and where even modest shifts in growth expectations or interest rate assumptions could trigger a disproportionate unwinding of recent gains.

Private Equity

Manufacturing cash as redemptions spill into Private Equity

Blackstone is reportedly preparing to package more than $2 billion of its leveraged buyout fund stakes into bonds via a collateralized fund obligation (CFO). (Source: Bloomberg; Reuters, June 8, 2026) This financial engineering allows the firm to generate liquidity without actually off-loading the underlying assets. It reflects a broader, rapidly expanding trend: Estimates show new CFO volume could rise 50% this year to over $30 billion as private equity sponsors struggle to exit investments made during the low-interest-rate environment of 2020 through 2022.

While securitizing fund stakes into debt tranches successfully unlocks fresh capital, it is ultimately a stopgap measure. When asset managers must resort to borrowing against their own illiquid portfolios to manufacture distributions, it underscores a gridlock in traditional M&A and IPO exit channels, indicating that returns for these pandemic-era allocations could face downward pressure.

This dynamic mirrors the concerns that recently drove waves of redemptions across private credit—namely, investor anxiety over valuation opacity, duration mismatch, and the realization that delayed realizations and "mark-to-model" pricing cannot create distributable cash in a frozen exit market. Similar to what we’ve seen in Private Credit, Private Equity is now coming to grips with elevated redemptions—with one private markets investment firm recently forced to cap withdrawals on one of its evergreen vehicles at 5% of net asset value after second-quarter redemption requests spiked to an estimated 9.8%.

Market

We have all been watching many 10%+ daily moves in large-cap stocks this year, with volatility more expected of small-cap investing. As markets continue to digest AI developments, geopolitical tensions such as the Iran War, IPOs and interest rate recalibrations, we have seen a less uniform market than at any point since 2000 and more than the financial crisis. For investors, this combination of elevated volatility and narrow leadership suggests greater sensitivity to shifts in sentiment, where momentum can reverse quickly and positioning becomes more important.

Economic Calendar: Week Ahead (Eastern Time)

Mon, 6/15 @ 8:30 am: Empire State Manufacturing Survey

@ 10:00 am: NAHB Housing Market Index

Tues, 6/16 @ 8:30 am: Housing Starts

@ 8:30 am: Import Prices

Wed, 6/17 @ 8:30 am: Retail Sales

@ 10:00 am: Manufacturing & Trade: Inventories & Sales

@ 2:00 pm: U.S. interest rate decision

Thur, 6/18 @ 8:30 am: Weekly Jobless Claims

@ 8:30 am: Philadelphia Fed Business Outlook Survey

@ 10:00 am: Leading Indicators

The Team Behind Friday Focus

Mary Ahn

Investment Research and Portfolio Strategy Manager

Cal Jones, CFA

Managing Director of Fixed Income

Eric Speron, CFA

Managing Director of Equities

Alton Tjahyono, CFA

Sr. Investment Strategist