9 minute read

The U.S. stock market reached new highs in the first quarter with three consecutive months of positive returns capping the quarter with strong gains for U S and International equities. The U.S. economy remained resilient despite short term interest rates sitting near 20-year highs. Strong corporate earnings, a robust labor market and the continued strength of the U.S. consumer provided a supportive backdrop for stocks and propelled the market to record highs.

The S & P 500 Index continued to reach new highs, gaining 10.6% in the 1st quarter. Large-cap stocks (S & P 500) outperformed small-cap stocks (Russell 2000 Index), and growth stocks (Russell 1000 Growth) again beat value stocks (Russell 1000 Value). The equally weight S & P 500 returned 7.9%, trailing the cap-weighted index by about two and a half percentage points in the quarter. Developed International and emerging market stocks also posted gains but did not keep pace with the U.S. market. Developed International stocks (MSCI EAFE) gained 5.8%, while emerging-market stocks (MSCI EM Index) posted a 2.4% return. Japanese stocks (MSCI Japan) were the standout performers in the quarter, gaining over 11% in dollar terms.

In the bond markets, returns were mixed in an environment where the benchmark 10-year treasury yield rose from 3.88% to 4.20% as markets reduced their expectation of Federal Reserve rate cuts from more than 150 basis points to just shy of 70 basis points (April 3) for the year 2024 and adjusted the start of the easing cycle from March to June. The Bloomberg U.S. Aggregate Bond Index declined .8% while high yield bonds were positive in the quarter.

Finally, our alternative strategies which include real estate, private credit and equity performed well in the quarter and were right in line with our expectations.

We are pleased with our Global Asset allocation strategies as most have outperformed their strategic benchmarks for the quarter, though we cannot guarantee this will continue. Returns were strong across the board, with higher returns from our most growth-oriented strategies as would be expected in a strong period for equity returns.

The sharp 1st quarter rally was driven by a resilient U.S. economy and strong corporate earnings. All eyes remain on Fed policy and falling inflation. When will the Fed start to cut, by how much, and why? The Fed has indicated that they plan on cutting interest rates three times this year, winding down the war on inflation.

Macro Outlook

The U.S. economy has continued to prove resilient despite the Fed maintaining a higher level of interest rates for longer than most expected. The main driver of this better-than-expected economic growth has been the continued strength of the U.S. consumer. The combination of robust job gains and steady positive real income growth has allowed consumers to continue spending despite higher rates. The strong economy has also benefited corporate earnings. And after a decade of near-zero interest rates, companies are generally well positioned financially with balance sheets that are healthier than they have been past tightening cycles.

The real GDP growth estimate (as of April 1st) for the first quarter of 2024 is expected to be 2.8%. If the growth rate holds, it would be the seventh consecutive quarter of economic growth. A recession is unlikely in 2024. We think the biggest risk will come from weakness among consumers in the latter half of the year and we will continue to closely monitor economic data and adjust our views accordingly.

Inflation and Interest Rates

There’s an old saying about Federal Reserve rate cycles; the Fed takes the escalator up and the elevator down. Because of the harmful impact higher rates has on the economy, the Fed is usually more methodical when hiking rates. On the other hand, the Fed has historically been more aggressive when cutting rates, especially when combatting recessions. This time is different.

Given the pandemic, related surge in inflation, the Fed embarked on the most aggressive tightening cycle in more than 40 years- moving the fed funds rate off the zero bound in March 2022. With 11 hikes overall between then and last July – and four consecutive 75-basis point hikes therein- the Fed clearly took the elevator up. With the Fed in “pause” mode for now, attention has turned to the coming rate cut cycle. The rub is the lack of cooperation by inflation data, which has been sticky this year and not yet at the Fed’s 2% target.

Inflation looks to still be trending lower, but a relatively stubborn decline will likely push the Fed to start cutting rates later and slower than expected. To be sure, we think the Federal Reserve will be cautious with the timing and magnitude of rate cuts. We are currently in line with consensus expectations the Fed will cut by 25 bps in July with two more cuts later in the year. But with inflation remaining above the 2% target, cutting too early could create a second wave of inflation, but waiting too long could put pressure on the consumer and lead to a recession.

We think the Fed does some fine tuning of rates without implementing the type of broad policy shift to which we become accustomed (the escalator instead of the elevator). If a recession does occur later, the Fed will have the ability to swiftly and meaningfully cut rates given current levels. For now, U.S. economic data seems supportive of growth not contraction. We continue to believe the Fed has the upper hand on inflation and we will see inflation grind lower albeit at slower pace in the near term. We continue to monitor inflation trends, the Federal Reserve’s decisions, and the government’s use of fiscal policy which will all play an important role in the outlook for inflation. We believe rate cut expectations will be a moving target as relevant data (both inflation and labor market) is released.

What about Political Risk?

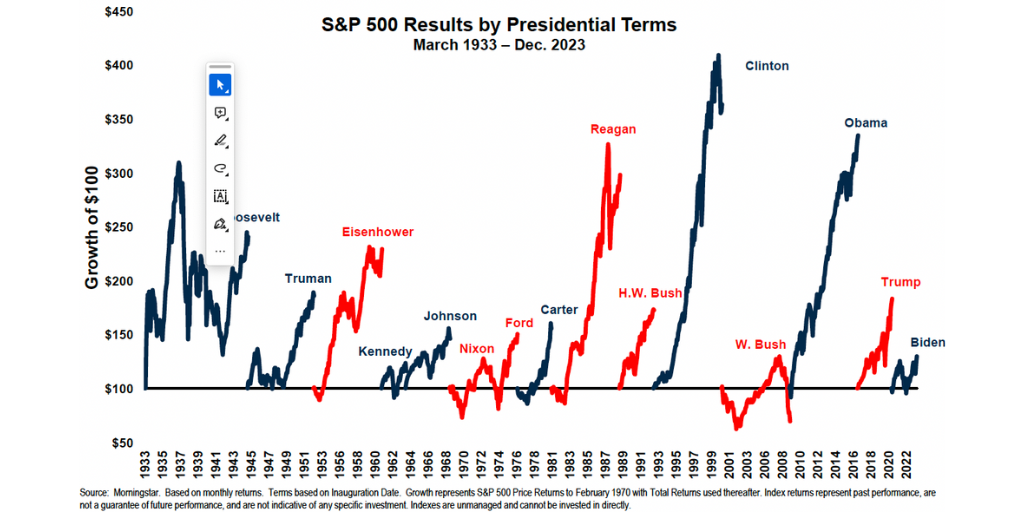

Since this is an election year we have had many questions about the presidential election. We stated in our article last month titled "A Piece of the Puzzle," by Mike Chen that the traditional viewpoint is that the Republican Party is better for business and hence may portend better performance in the stocks markets. Is this really true in practice, though?

As one can see in the chart below, both Republican presidents and Democratic presidents have experienced overwhelmingly positive stock market performance. In fact, since the inception of the S&P 500 index 91 years ago, the two presidents with negative stock performance after having left office were from the Republican party:

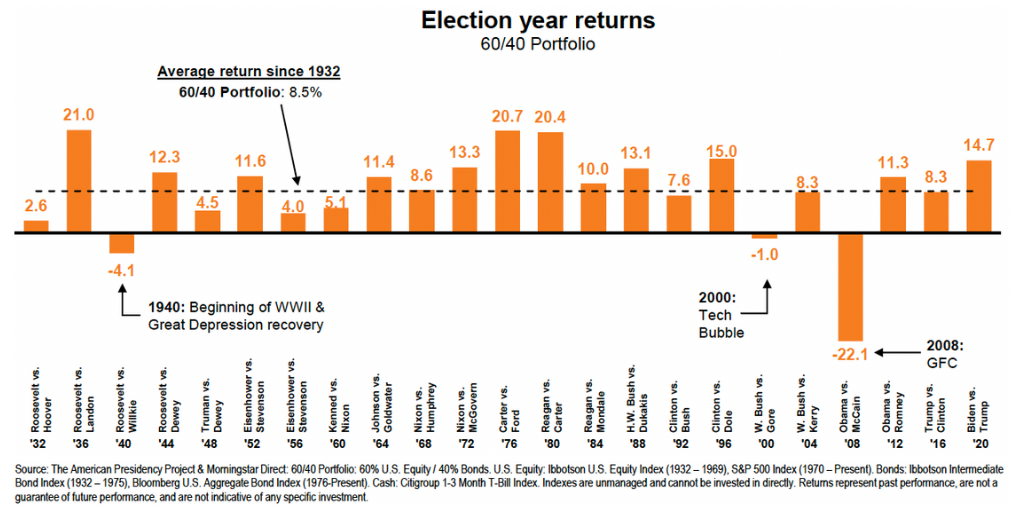

Perhaps another way of looking at historical returns during an Election Year is to see how actual portfolios would have done in past election cycles. Once again, the evidence is clear that “staying the course” has worked out well compared to trying to market time the election cycles.

During election years, a “60/40” portfolio has delivered an average annual return of +8.5%, with 87% of those years having had a positive return. Only three years experienced negative occurrences; each of those were macroeconomic related:

Financial Market Outlook

In November, the Fed made it clear they believe the end of the war on inflation is near, and not only are they preparing take their foot off the brake, but they are also anticipating interest rate cuts in 2024. At the same time, the Fed also said it foresees the economy remaining relatively healthy with steady growth and modest levels of unemployment. Historically, the end of the fed’s hiking cycle usually serves as a tailwind for stocks.

U.S. equity markets rose in the quarter as earnings growth exceeded expectations. The growth was mainly due to large-cap growth stocks, a trend that has been in place since 2023. Confidence in earnings did not sour despite rising rates, which could have had a negative impact on stock valuation. Smaller cap stocks were again not able to keep pace with larger cap companies and remain relatively cheap. Although small-caps appear cheap relative to large-caps, our portfolios have a slight overweight to large cap. We do think, however that small cap stocks will close the performance gap as the year progresses and market returns will broaden out and areas of the market that have significantly lagged will perform much better.

We think the backdrop for equities looks favorable and that U.S. stocks can continue to climb the wall of worry. At the same, we fully acknowledge there are metrics to suggest some caution, mainly valuation. Looking ahead, we think equities will need better earnings growth to move much higher. Current economic data points suggest continued economic growth with potential rate cuts which point to good earnings growth. We expect another year of positive returns for U.S. equities.

Our overall equity allocation also favors another unloved part of the market – developed international stocks. While much of the talk is about continued U.S. outperformance, the average international stock outperformed the average U.S. stock last year. This year the MSCI EAFE Index is up a respectable 5.78% and MSCI Japan Index is up over 11% leading the way. We think international developed equities will continue to do well and will close the performance and valuation gap versus the U.S. market. Our equity strategy is to remain fully diversified among U.S. large cap, mid cap and small cap equities while also investing in developed international equities with an underweight in emerging market equities.

Fixed Income

Inflation and Fed policy will continue to be the major drivers of the bond market in 2024. All eyes are on the Fed when it comes to fixed income. At the Fed’s late march meeting, Chair Powell announced that rates would remain unchanged at the current 5.25%-5.5%, keeping it at the highest level in over 20 years. This was the fifth consecutive meeting that rates were held steady, and this outcome came as no surprise, particularly after the most recent inflation and employment data, both of which came in stronger than expected. For fixed income investors, the belief that the next change in policy is a rate cut instead of a rate hike is more important than how many rate cuts we get this year. We think the Fed will cut rates and we will finally get back towards a normal shaped yield curve, with the front end of the curve declining more than the long end. Our thinking is based on our views of near-term inflation grinding lower, Fed policy becoming too restrictive and the consumer slowing down and comments from policy makers.

For now, investors can continue to benefit from higher short-term yields. The Aggregate Bond Index is yielding 5% which is above the current in 3.5% inflation rate. So, bonds finally provide a positive real (after inflation) yield. Core bonds offer good return potential with downside protection. We favor treasuries, long term municipal bonds and high-quality credit issues.

Alternative Strategies

Alternatives can provide powerful long-term portfolio benefits and non-correlated returns to traditional stock and bond holdings and improve risk-adjusted returns of balanced portfolios. Given the current macro risks and market backdrop, we think they are especially valuable.

We favor private real estate investment allocations to multi-family, industrial and self-storage and selected grocery anchored centers for those clients that have the capacity to accept the risks and lack of liquidity inherent in private investments. We expect equity like long term returns from these investments with built in inflation protection and tax efficient income generation. We also favor private equity and credit opportunities and recently added a position in commodities. We will continue to add alternatives to our diversified balanced portfolios.

Closing Thoughts

The U.S. economy currently appears in good shape. The stock market continues to hit new highs as economic growth continues to benefit corporate revenues and earnings. We expect more volatility given the headline risks related to Fed policy adjustments and the presidential races. While challenging, it is critical to stay the course through these trying periods.

Outside of the U.S, stock market, we already see attractive medium-term expected returns from international and emerging stocks. A declining dollar, as we expect would further fuel non-U.S. equity returns.

We feel fixed-income assets and high-quality bonds are also now attractively priced with mid-single digit or better expected returns. Core bonds can also provide downside stability in the event of a recession. Our investments in alternative strategies should provide further resilience to our portfolio.

We sincerely thank you for your confidence and trust in us. Please do not hesitate to reach out to us if you have any questions or wish to discuss how all this relates to your specific financial situation in more depth.