7 minute read

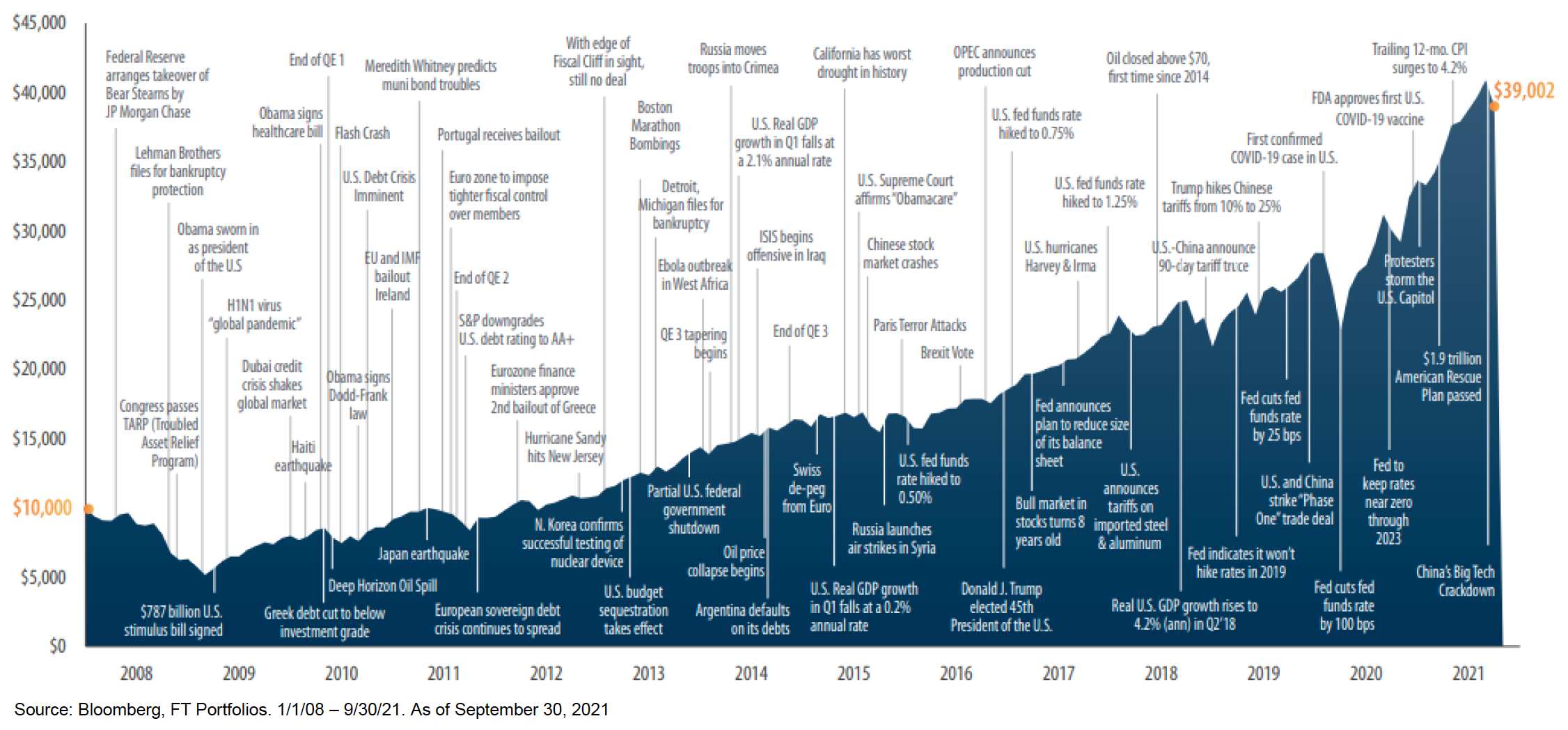

This year so far has been stellar for U.S. equity investors, as the S&P 500 was positive for seven consecutive months through August. September ended the winning streak as it closed with a whimper. This is not uncommon though: September is historically the worst month for stock performance on average since the index’s inception in 1928. From the S&P 500’s all-time high on September 2, the drawdown through the final day of the month was -5.1%, ending a streak of 211 trading days without at least a 5% pullback – the longest since January 2018.

Despite the September drop, the S&P 500 has had an impressive year with 54 new closing highs thus far, which is the fourth best on record. U.S. equities are up 15.9% for the year while international stocks as measured by the MSCI EAFE are up 8.3% and emerging market (EM) stocks are down 1.2% for the year. The drop in EM stocks is due to the double-digit declines in China driven by concerns about regulatory reforms. But the drawdown is in line with the longer-term average, and as the intensity of new regulations eases, this should provide some relief.

U.S. small cap stocks dropped 4.4% for the quarter but are still up 12.4% for the year as measured by the Russell 2000. Growth stocks beat value stocks for the second consecutive quarter. In the bond markets, the 10-year Treasury yield ended the quarter just slightly above where it began, at 1.53%. But it was a volatile quarter, with the yield initially plummeting below 1.2% in early August and then shooting back up in late September. The bond index was essentially flat for the quarter and slightly down (1.6%) for the year. Credit-oriented bond investments outperformed core bonds and are positive for the year.

Our global strategies have performed better than their benchmarks so far in 2021, however, there is no assurance as to future profits or that we will meet or exceed benchmarks in the future. Our overweight positions to U.S. equities in most of our strategies and our emphasis on non-core bonds and credit strategies have been beneficial. Our alternative investments also did well, with real estate leading the way. Overall, we are very pleased with our results for our strategies so far in 2021.

As we enter the home stretch of 2021, we look back to previous years as the fourth quarter historically has been the strongest seasonal period for stocks. For example, according to Ned Davis research, since 1970 the median fourth-quarter return for the MSCI World Index is 4.4%, and it has registered a positive return for the quarter more than 75% of the time. We believe this positive trend will hold up for the fourth quarter of 2021.

The U.S. and Global Macro Backdrop – Climbing the Wall of Worry

There was no shortage of risks conspiring to bring the market down a notch in September, including ongoing debt ceiling negotiations, fiscal policy uncertainty, monetary policy uncertainty (including over whether Jerome Powell will keep his position as Fed head), global supply chain bottlenecks, slowing economic and earnings growth projections, ongoing inflation fears, and concerns over Chinese regulatory reforms. The wall of worry is always present, and the 24-hour news cycle ensures it reaches you in one form or another. But we use proven investment processes and diligent research to block out the noise and make long-term investment decisions on behalf of our clients.

Of note, there were no major U.S. economic policy surprises during the quarter. On the fiscal policy front, it was business as usual: the Washington gridlock, infighting, and dysfunction. It remains to be seen what type of infrastructure spending and tax hike legislation emerges from Congress in the weeks ahead and how the federal debt ceiling standoff gets resolved. No matter what fiscal package is passed, the economy is now facing a fiscal drag – a negative impact on GDP growth – from the expiration of pandemic spending and support programs, which have boosted growth over the past several quarters.

On the monetary policy front, the Federal Reserve Open Market Committee (FOMC) announced at its September quarterly meeting that it is likely to begin tapering its $120 billion monthly quantitative easing (QE) asset purchases starting in November, with the objective of concluding the process and ending QE “around the middle of next year,” according to Fed chair Jerome Powell. This was broadly in line with market expectations.

The FOMC’s updated forecasts for growth and inflation reflect the evolving economy. The Fed sharply lowered its median GDP forecast for 2021 to 5.9% from 7% in June, a function of the delta variant–driven growth slowdown during the summer and ongoing production shortages and supply chain bottlenecks (semiconductor and shipping container shortages). Although global and U.S. economic growth rates slowed in the third quarter, they are still solidly above trend in the near term, so risk of a recession remains low – absent an exogenous shock.

Meanwhile, along with reducing its 2021 growth forecast, the FOMC sharply increased its median core inflation forecast for this year to 3.7%, up from 3% in June, pointing to ongoing supply-side disruptions. The Fed also slightly boosted its projections for core inflation in 2022 and 2023. We are still in the camp that believes inflation trends are rising, but they are mostly transitory and not permanent.

On the interest rate front, we think the odds are still high that short-term rates will gradually rise over time but will remain low by historical standards and also below the rate of inflation for several more years. Monetary policy will likely remain accommodative and broadly supportive for risk assets.

Financial Market Outlook

Moving from the macro to the markets, we see the strongest likelihood for continued positive returns for equity and credit markets or risk assets in general. This will be driven by continued economic and corporate earnings growth (though decelerating in the United States) and supported by still-accommodative monetary and fiscal policy, albeit less so in the United States. The 10-year Treasury yields are likely to rise although we don’t expect a sharp increase, which means a poor environment for core bond returns, both in absolute terms and relative to other asset classes and alternative strategies.

We expect international and EM stocks to outperform the S&P 500, due to their sensitivity to global growth, their larger potential for earnings acceleration from still subpar levels that have lagged the U.S. recovery, and their much lower starting equity market valuations. Therefore, we see potential for strong returns from both a cyclical earnings rebound and increased valuations in foreign stock markets over the coming years. International stocks are trading at a record valuation disparity to U.S. stocks.

A new cycle of economic expansion could bring new leadership by international stocks relative to U.S. stocks, supported by better-than-average global growth and lower stock valuations. Covid-19 concerns have weighed on the global growth outlook, prompting a rotation this summer to U.S. equities. However, signs that the delta variant may not derail growth could mean a rotation back as economic growth accelerates this fall. European stocks have done well this year while EM has lagged, driven by Chinese market concerns. All of this underlines the importance of global diversification, as market leadership and trends can change quickly.

For the U.S. market, with valuations stretched, we see little room for valuation expansion. Earnings growth should be the primary driver of U.S. equity returns. We expect single-digit returns rather than the robust returns of the past two years.

Despite the expected weak August and September jobs report, the Federal Reserve will likely slow the pace of its bond purchases this year. Since March 2020, the Fed has been purchasing Treasuries and mortgage-backed securities to support the economy – by buying bonds, it puts cash into financial markets and helps keep longer-term yields low. We expect a tapering announcement in November. We don’t expect the Fed to raise rates before late 2022 or 2023. As a result, we expect low returns from fixed income. We do expect solid returns from real estate, private credit, infrastructure, and other alternative investments over the next several years.

Portfolio Positioning

Even though we have been watching things very closely, we made no major changes to our portfolio allocations in the third quarter. They remain well-diversified and balanced across a range of global asset classes, risk factors, and investment strategies, each of which has different expected performance.

We believe the portfolios are well-positioned to generate relatively strong returns in our most likely baseline scenario of a continued global economic recovery with moderately rising interest rates and inflation and decelerating growth in the United States. And our balanced portfolios should also prove resilient if we have an inflation or growth scare.

In terms of our overall risk exposure in our globally diversified moderate portfolios, we are overweighting equities relative to bonds. The relative valuation of U.S. stocks versus bonds is attractive, and even more so for foreign stocks. Despite high absolute U.S. stock valuations, stocks look relatively cheap at a 5% earnings yield when compared to a 1% Treasury bond. We also see tactical opportunities in foreign stocks as their economies accelerate.

We believe Treasury rates will be pressured higher from current levels due to stronger global growth and reflation. As a result, we favor short-term credit strategies over core bonds. We have a bias toward reflationary assets, and in our alternative investments we own real estate, infrastructure, and commodities as portfolio diversifiers and risk reducers that will do better if inflation rises.

Closing Thoughts

We are keenly focused on the post-pandemic economic and inflation landscape. The recent moves up in inflation and down in growth forecasts have been driven by the combination of supply and demand shocks and dislocations. Given the overall positive trend in the fight against Covid-19, we do not expect it to derail the global economic recovery in the coming years. Monetary policy, interest rates, government policy, and the economic and earnings growth cycle remain broadly supportive of equity and other risk assets.

We expect a solid fourth quarter and 2022 for economic growth. We believe our portfolios are well-positioned for further gains as the U.S. and global economies continue to recover. We expect solid returns from global equities and our alternative investments. As the macroeconomic environment evolves, we will tactically adjust our portfolio exposures based on our assessment of risk and potential returns.

As always, there are more questions than there are answers, but our team stands ready to help. We thank you for your continued confidence. We are passionate about helping you achieve your goals.