We sincerely hope you and yours are healthy and adjusting well enough to all the disruptions and changes we are currently facing together in our daily lives. We will surely remember this time and the profound impact it is having on our families, communities, and country.

We will get through this crisis. Things will improve, and we will recover. This too shall pass. In the meantime, events are moving very rapidly, policy responses are in flux, and markets are extremely volatile.

As we adapt as best we can during this unprecedented and uniquely challenging period that is riddled with uncertainty, we are all, understandably, feeling the effects in our own way and at various intervals. We are here and ready to do our best to answer any questions you may have or to simply talk things through at times when you feel it may be helpful. We can navigate this current together; we are here for you.

First Quarter Market Update

The first quarter of 2020 has been an unprecedented period in U.S. financial market history across numerous dimensions:

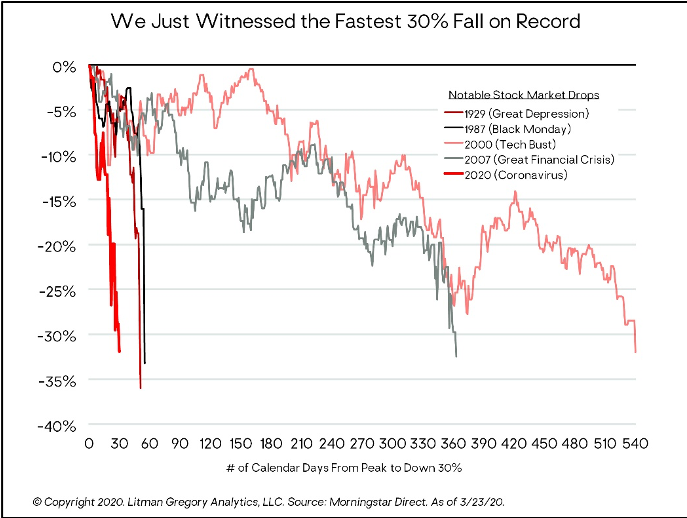

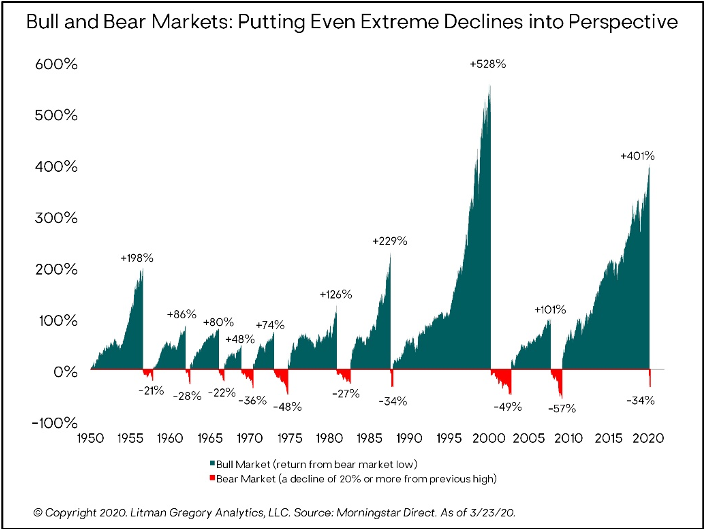

- The U.S. stock market fell into a 20% bear market in the shortest time ever—just 22 days—and continued further, dropping 30% in a record 30 days. The typical historical bear market peak-to-trough decline has taken around 12 to 18 months.

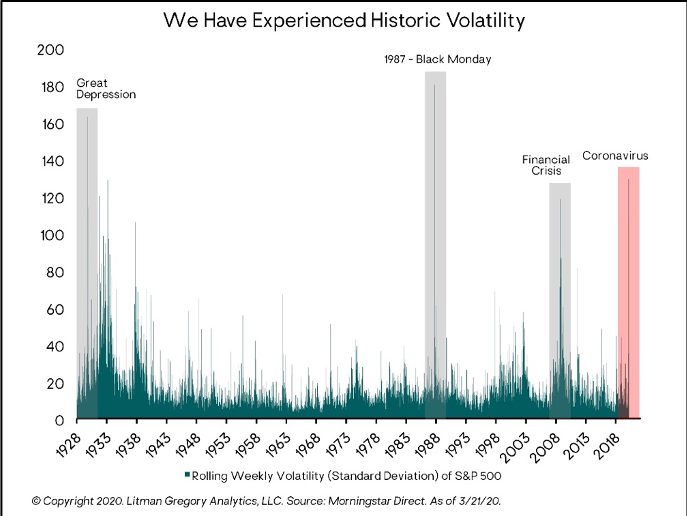

- Short-term expectations of stock market volatility, as measured by the VIX index—often referred to as the market’s “fear index”—closed on March 16 at an all-time high in its 30-year history. And the market’s actual realized volatility has been higher only in October 1987 (on Black Monday) and the late 1920s.

- The 10-year and 30-year Treasury bond yields fell to all-time lows of 0.54% and 0.99%, respectively, on March 9.

- Oil prices had their biggest one-day drop since the 1991 Gulf War, plunging 25% on March 9, triggered by a price war between Saudi Arabia and Russia.

Larger-cap U.S. stocks fell 20% this quarter. Growth stocks have continued to hugely outperform Value: the Russell 1000 Growth Index fell 14%, while the Russell 1000 Value Index fell 27%. Smaller-cap U.S. stocks did even worse, falling 31%.

Developed international stocks and emerging-market stocks both dropped approximately 24%. Much of the differential between U.S. and foreign stock market returns has been due to the appreciation of the U.S. dollar, which has risen roughly 2.5% year to date.

In the fixed-income markets, core bonds gained just over 3%, once again playing their key role as portfolio ballast against sharp, shorter-term stock market declines. As noted above, Treasury bond yields have fallen sharply. They have been extremely volatile as well—shooting up on some days when stocks were also sharply selling off. The 10-year yield ended the quarter at 0.70%, down from 1.92% at year-end.

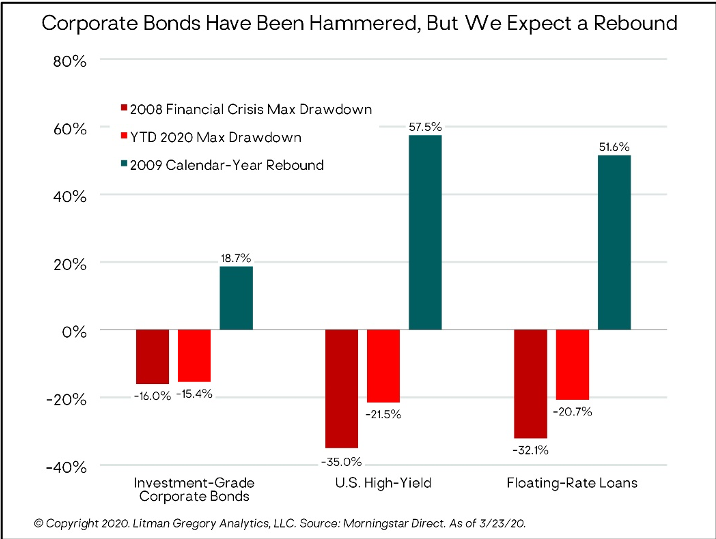

Turning to the credit markets: Floating-rate loans and high-yield bonds took it on the chin, with both dropping around 13%. But investment-grade corporate bonds were far from immune, having lost over 4%.

The losses so far for high-quality investment-grade corporate bonds are right on par with the 2008 financial crisis. And this time the drawdown happened in just 10 days, compared with nine months in 2008. This gets to the heart of the Federal Reserve’s massive policy response. It is throwing everything it can at supporting bond markets to prevent them from freezing up and spiraling into an economic crisis.

The good news is that by their nature, bonds have a narrower range of return outcomes than stocks do. So we definitely view these as short-term drawdowns and not permanent losses of capital. Our bond funds are run by skilled, experienced managers. Most of them were relatively defensively positioned coming into March because yields were low and the managers weren’t being well compensated for taking on credit risk. Despite that, their fund returns have been hammered this month. But we believe this has created some great buying opportunities for them to put some of their cash to work at much more attractive expected returns. So we are excited about that.

And as a reminder, in 2009 as the financial crisis began to ease, there was a huge snapback as well as very high returns but there is no guarantee of this repeating.

Update on the Macro Outlook

Coming into the year, we saw the potential for a moderate rebound in the global economy (especially outside the United States) on the back of reduced U.S.-China trade tensions and extensive global central bank monetary accommodation. And in January and early February, there were signs the manufacturing sector had bottomed and a nascent global recovery was indeed underway. Stock markets rallied to all-time highs.

However, the arc of the coronavirus and the increasingly aggressive U.S. and global response to try to slow its spread has drastically changed everything. Our base case now—and it seems most investors, economists, politicians, and central bankers agree—is that the U.S. economy is headed into recession in the second quarter. It is likely to be a severe one, with a sharp contraction in GDP and an unprecedented rise in unemployment and jobless claims.

The consensus also appears to be that the recession will be short in duration, with a rebound beginning around the third quarter. But this is by no means a sure thing. To the extent equity markets are not fully discounting a more severe outcome, downside risk remains.

The depth and duration of the recession—and the strength and timing of the ensuing recovery—depend on two key variables:

- The progression and spread of the virus: how effective our medical response and social-policy efforts are in flattening the curve

- The fiscal, monetary, and regulatory policy response: how quick and effective new policies will be in supporting households, businesses, and financial markets—mitigating the short-term recessionary damage and preventing a downward spiral into something much worse than a severe but short recession

The effectiveness of the medical response and economic policies (and their impact on human behavior at the societal level) will help answer the fundamental economic questions of how severe and how long the economic downturn and recession will be. And the answers to these economic questions will help answer the investment questions of how severe and how long the equity bear market will be.

The financial markets and the real economy are interconnected—each drives the other and can reinforce or magnify a trend in one direction. A rebounding stock market supports the real economy and vice versa through positive wealth effects, increased incomes, profits and spending, risk-taking, and optimism. But they can also feed off one another on the downside, in a self-reinforcing negative spiral that can ultimately lead to an economic depression if the spiral is not broken.

We expect financial markets to react positively at the first signs of a flattening in the number or rate of new daily coronavirus cases reported, as we saw happen in China in February, and as also happened during the SARS epidemic in 2003.

Italy might be a leading indicator of the progression of the virus in other developed countries. Many experts have said the U.S. virus situation is roughly two weeks behind Italy’s. But there are also important differences between the two countries (e.g., medical infrastructure, demographics, policy response) that make this an imperfect comparison.

On the Economy

The near-term economic damage from the United States’ and other countries’ responses to the virus now looks almost certain to be severe (barring some unexpected major medical breakthrough in the near future).

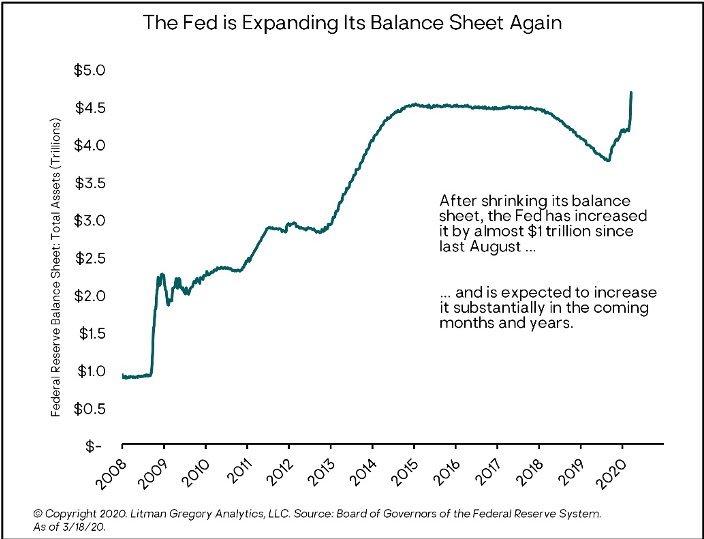

On Sunday, March 15, the Fed held an emergency meeting where it cut the federal funds rate by one percentage point to near zero. The Fed also announced it was restarting quantitative easing (QE) with at least $700 billion in planned purchases of Treasury bonds and mortgage-backed securities.

At his press conference following the meeting, Fed chair Jerome Powell said GDP growth was likely to be negative in the second quarter, and beyond that the economic outlook was highly uncertain, as it depends on how widely the virus spreads: “I would say, in fact, unknowable.”

Over the following week, economist after economist slashed their second quarter GDP forecasts deeper and deeper into contractionary territory. Forecasts may have changed again by the time this is published, but to give a sense of the magnitude, going into the last week of March, Goldman Sachs was forecasting a 24% annualized decline, Morgan Stanley a 30% decline, JPMorgan a 14% decline, and both Bank of America and Citigroup a 12% decline, to name a few. For comparison, the worst quarter during the 2008 financial crisis was an 8.4% annualized GDP contraction, in the fourth quarter of 2008. (As of quarter-end, Goldman Sachs, for one, has already revised its second quarter GDP forecast to a 34% decline.)

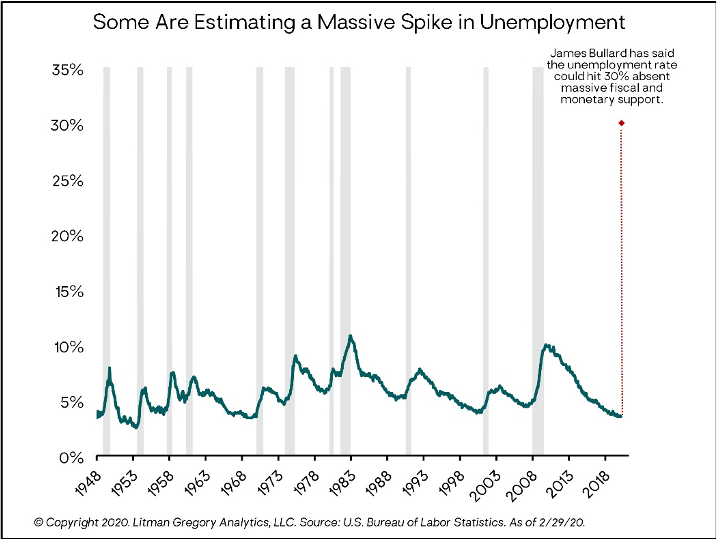

On Sunday, March 22, Federal Reserve Bank of St. Louis President James Bullard topped them all. He was quoted by Bloomberg News as citing the potential for a 50% quarterly drop in GDP and a 30% unemployment rate in the second quarter, in the absence of massive fiscal and monetary policy support.

Bullard also said that with an aggressive government response, economic activity should begin to bounce back in the third quarter. And the fourth quarter of 2020 and the first quarter of 2021 could be “quite robust” as Americans make up for lost spending. “Those quarters might be boom quarters,” he said. As another example, Goldman Sachs forecasts a 19% growth rate in the third quarter, following its expected 34% second quarter plunge (forecast as of 3/31/20).

As mentioned earlier, an economic slowdown—particularly an extremely sharp one due to extreme virus containment efforts—can quickly morph into a self-reinforcing negative spiral. Consumers cut back spending, businesses lay off workers, unemployment rises, incomes drop further, spending drops further, corporate profits drop, companies and households default on loans, companies go out of business, investment and employment drop further, etc., causing an even deeper and longer recession (if not depression) and bear market.

In the case of such a severe external shock, the government’s economic policy responses are critical. There are two main levers: monetary policy (central banks) and fiscal policy (government spending, tax cuts, unemployment insurance, loans, debt forgiveness, etc.).

One lesson learned from the 2008 financial crisis is this: When it comes to the policy response, go big and go fast. Time is of the essence (just as it is with the virus response). Governments need to make a credible commitment to “do whatever it takes” to support the economy and prevent the negative spiral from taking hold.

Monetary Policy

The Fed and other major central banks seem to be all-in to support the fluid functioning of credit, lending, and financial markets, as well as fulfill their critical role as the “plumbing” of the real economy.

As noted above, at an emergency meeting on Sunday, March 15, the Fed cut the federal funds rate to near zero and restarted QE. A week later, it increased the QE program from “at least $700 billion” to essentially an unlimited amount in order to keep interest rates and borrowing costs low. The Fed also initiated a number of programs—going beyond the tools it enacted during the 2008 financial crisis—to try to ensure enough credit, loans, and liquidity are flowing to banks, businesses, households, and the overall global financial system. It is likely the Fed will do still more (e.g., increasing its asset purchases to support the huge fiscal stimulus that is coming or even effectively monetizing the debt or “helicopter money”). Other major central banks are also starting to pull out all the stops, and more will likely come until the crisis period ends (and maybe beyond).

Fiscal Policy

While extremely accommodative monetary policy is necessary, it is not sufficient to mitigate this economic crisis. Only fiscal policy can have a large enough and direct enough impact necessary to support and sustain individuals and businesses until the storm has passed and the virus containment measures show signs of working.

Congressional Republicans and Democrats and the Trump administration all seem to be in agreement that something massive needs to be done and done quickly. On March 27, Congress passed, and the president signed into law, a $2 trillion stimulus package. Similar support measures are being debated or implemented around the world. Discussions are continuing about additional steps to take in support of markets and the economy.

Public support and business support are also undoubtedly strong. So the political obstacles to getting something done should be relatively low, especially considering how polarized the current political environment otherwise is. There really is no alternative. And like the monetary policy response, the fiscal stimulus will also be global in scale, with even austerity hawks like Germany now acceding to its necessity.

The fact that almost everyone across the political, ideological, and economic policy spectrums agrees that the aggressive measures necessary to slow or contain the virus could tip the U.S. and world economies into a depression, is good news. It greatly improves the odds countries will act quickly and forcefully to enact fiscal, monetary, and regulatory policies to prevent that dire outcome from happening.

Current Portfolio Positioning

We are dealing with disruption on an unprecedented scale. In this highly uncertain environment, we will focus on a defensive approach at a time of heightened volatility and be offensive as prices overshoot to the downside. As always, we remain focused on meeting our clients’ longer-term financial goals and objectives while managing and balancing nearer-term risks.

In our balanced accounts, we will focus on U.S. large-cap equities with strong balance sheets. In spite of the relative outperformance of U.S. large-cap equities, we see room for further outperformance as these companies are in the best position to weather this storm. As markets drop further, we will analyze at which point we would want to add another increment to U.S. stocks.

We are maintaining our positions in European stocks and emerging-market stocks because their expected returns have also gotten much more attractive on a forward-looking basis after their recent price declines. And unlike U.S. stocks, we believe they were already at relatively attractive valuations and offered attractive expected returns prior to the virus-related selloff. We will not look to add to this position, as we feel U.S. stocks offer better risk and reward when compared with international equities.

We will look to opportunistically add to high-quality segments of the fixed income markets when we see dislocation. U.S. corporate, mortgage-backed, and municipal bonds have been negatively affected during these extreme conditions. We will look to redeploy into these attractive categories. Meanwhile, we remain cautious on the weaker segments of the high-yield market.

Lastly, we will opportunistically invest in real estate and infrastructure assets.

Closing Thoughts: This Crisis Will End. This Too Shall Pass.

It is so important for us as investors to maintain our focus on our long-term financial goals and objectives. As hard as it may be, from an investment perspective we need to try to look through the current environment of fear and concern—emotions which, given the circumstances, are totally justified and felt by all of us—to the almost certain outcome of the virus crisis receding and economic recovery occurring.

Throughout history, the world has faced numerous severe challenges and economic downturns and has always come out the other side. While not minimizing the unique risks and unknowns from the current crisis, we will bet on that being the case again. There is a good chance the recovery may start happening before the end of the year.

As a long-term investor, trying to time market tops and bottoms is a fool’s game. The evidence is overwhelming that most investors diminish their long-term returns trying to do so. They are more likely to chase the market up and down, and get whipsawed, buying high and selling low. But incrementally adjusting portfolio allocations in a patient and disciplined fashion in response to changing asset class expected returns and risks makes a lot of sense for long-term investors.

The time to be adding to stocks and other long-term growth assets is when prices are low and markets—and most of us personally—are gripped by fear and uncertainty rather than complacency, optimism, or greed. Investing at such times will feel very uncomfortable. It may seem like the market could just keep dropping with no bottom in sight. But that is exactly where research, analysis, patience, experience, and having a disciplined investment process come most into play. Stay the course.

Again, we are here and ready to do our best to answer any questions you may have or to just simply talk things through at times when you feel it may be helpful. We can navigate this current together; we are here for you.