11 minute read

Overview

Ten-plus months into the year and I think it is fair to say that 2020 has been the most extraordinary year of our generation, and the events that unfolded around the world have certainly made their mark on the U.S. financial markets. As you likely recall, the U.S. stock market plummeted in the first quarter, but what you might not so vividly remember is that the market fell into a 20% bear market in the shortest time ever – just 22 days – and continued dropping 30% in a record 30 days. There was talk of a depression, and nightly news reports showed imagery of cities literally shut down as people began to queue up in food lines reminiscent of the 1920s. Yet equity markets have staged a remarkable rebound since March. The S&P 500 index rose 8.9% in the third quarter, has recovered all its losses for the year, and is now in positive territory for the year – up 5.5%. It is worth noting, however, that even though smaller cap stocks posted a return of 5% for the quarter, they remain negative for the year.

Mega Returns

The mega-cap growth companies continue to lead the market and have pulled investors out from the depths experienced just six months ago. The often-referenced FANMAG group of stocks (Facebook, Amazon, Netflix, Microsoft, Apple, and Google parent Alphabet) are up an astonishing 42.5% year to date. By comparison, the price return for the S&P 500 is 4.1%. And excluding the FANMAG stocks, the other 494 names in the index have a 3.6% loss year to date (source: Ned Davis Research).

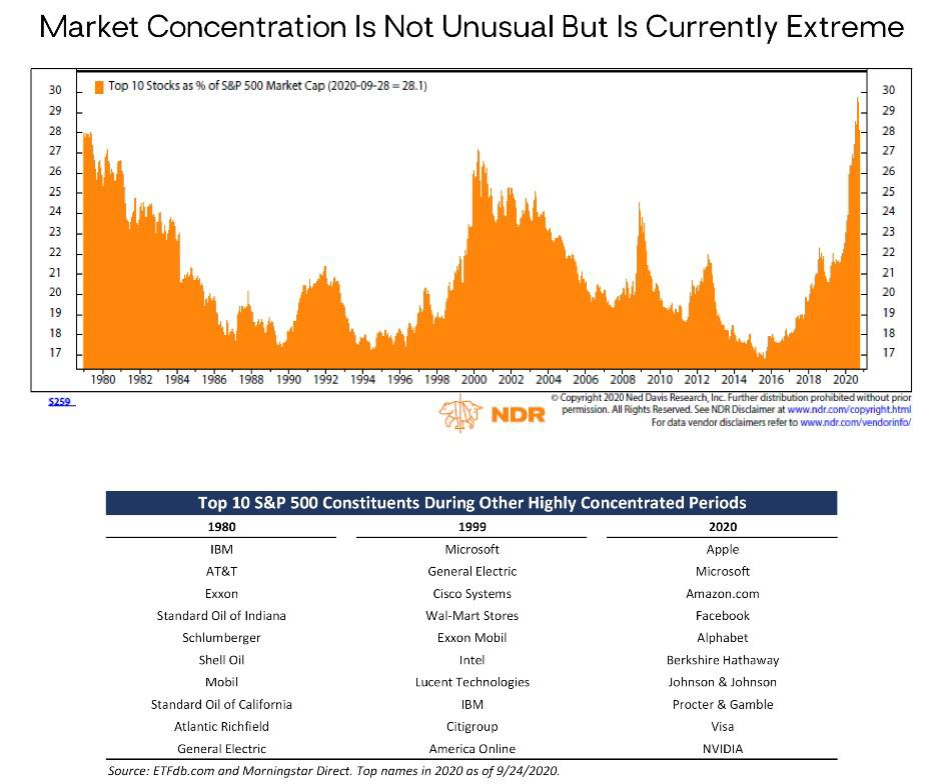

The strong performance of these top index names means concentration within the index has soared to new highs. The top 10 stocks in the S&P 500 make up a record 28% of the total market cap of the index.

But it is worth noting the top names in the index have constantly changed throughout history. Back in the 1980s, oil and gas companies dominated the top 10. In the late 1990s, it was technology companies that held the top position – Microsoft is the only one still in the top 10 today. Now, the FANMAG stocks are in the pole position.

For further historical context, it is not out of the ordinary for a handful of companies to make up a significant percentage of the index. Keep in mind that the outsized returns posted by these companies in the past have come from their ascension up the market cap spectrum, not from owning them once they are at the top of the mountain. Also interesting is that the strong performance of growth and technology companies relative to value companies continues. Despite pundits proclaiming growth stocks peaked in 2019, the outperformance of growth that started in 2007 has accelerated at a pace not seen since 1999-2000.

All this hype might lead you to believe that the markets are overly frothy, yet the fundamentals of the firms in the S&P 500 are unprecedented. The current firms score high marks in terms of economic value created, revenue growth, establishing new markets, and disrupting old players. And in an environment where growth has been scarce, with interest rates at all-time lows, investors have been willing to pay up. Valuations on these mega-cap stocks are indeed high, but we believe they are much more reasonable today than they were during the dot-com bubble, especially when adjusted for current market conditions. The mega-cap growth effect is driving not only the results of growth versus value in the United States, but also the relative returns of U.S. stocks versus foreign stocks. For the third quarter, developed international stocks gained 6%, which is almost 300 basis points behind U.S. stocks (MSCI ACWI Index, ex U.S.). However, emerging market stocks outperformed U.S. stocks with a return of 9.65% (MSCI Emerging Market Index). Our international investments have performed better than their respective indexes for the quarter and for the year, of course there’s no guarantee of this continuing going forward.

International

Year to date, the 11% outperformance of U.S. large cap stocks relative to foreign stocks (represented by the MSCI ACWI, ex U.S.) can be attributed to the mega-cap growth stocks. For the year, the MSCI ACWI, ex U.S., has lost 5.4% while the S&P 500 equal-weighted index has roughly the same performance with a 4.7% loss. Meanwhile, as mentioned, the market cap-weighted S&P 500 is up 5.6% this year. We have seen solid positive performance from both our U.S. investments and our international investments.

Fixed Income

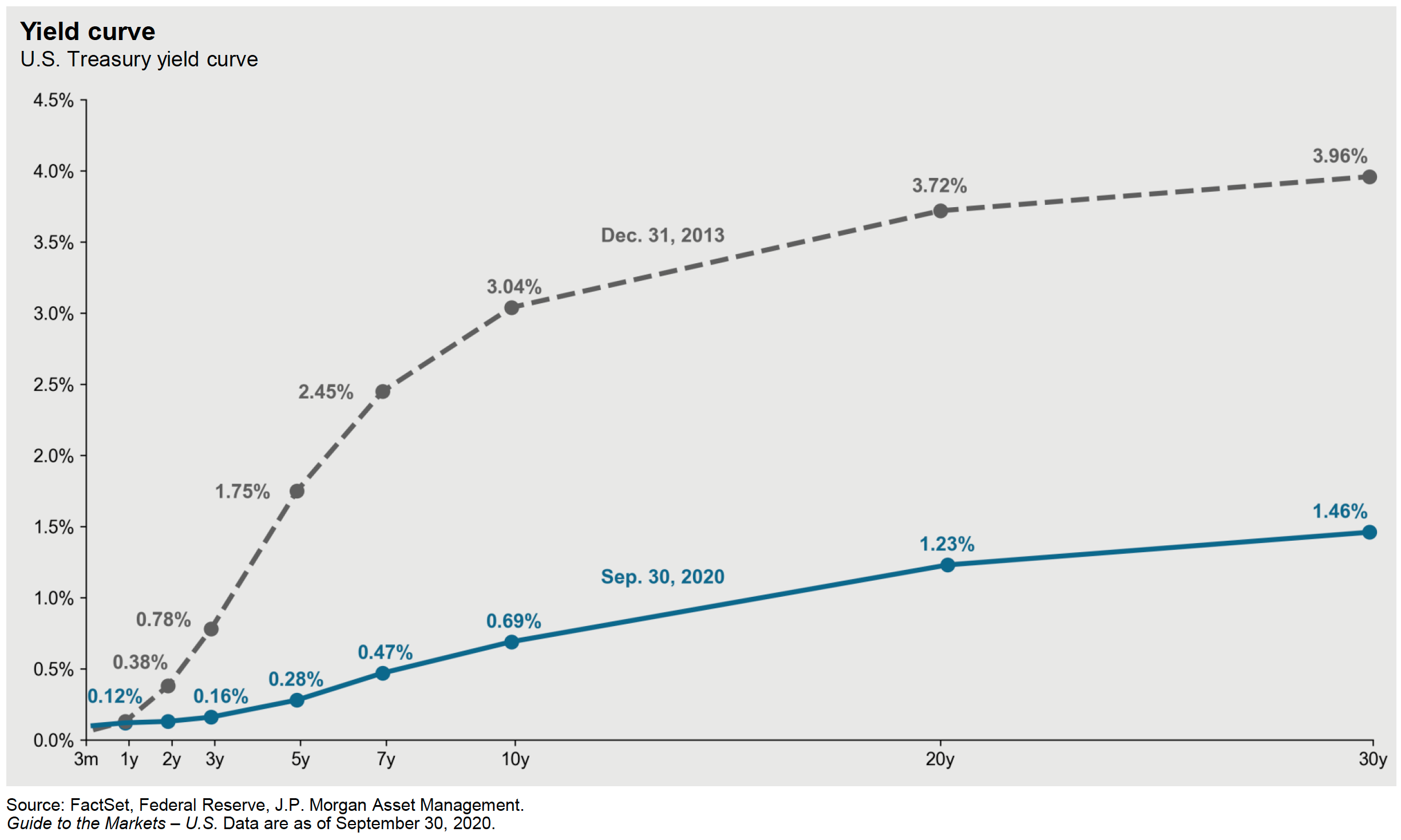

Within fixed-income markets, core bonds gained 0.6% for the third quarter (Barclays Aggregate Bond Index). Treasury yields were unchanged over the past three months. Investment-grade corporate bond spreads narrowed slightly over the quarter, as did spreads for high-yield bonds. This led to gains for credit strategies, each rising anywhere from 1% to 5%, with high-yield bonds leading the way. We are pleased with our fixed-income results for the quarter.

Bond markets have been calm throughout the summer, thanks in large part to extremely accommodative monetary policy from the Federal Reserve. Fed officials have signaled that they do not expect to raise rates at least through the end of 2023. With a new policy of “average inflation targeting” around 2%, coupled with inflation that has rarely topped that level over the past decade, many market participants are expecting low rates and supportive monetary policy to continue for a long time to come. Accordingly, we expect rates to remain low for several years.

The Optimistic Pessimist

Looking out over the next several quarters, we see several reasons to remain cautiously optimistic about the investment prospects for global equities and other risk assets. We highlight them below.

Reasons for Optimism

The economic recovery is underway. An economic recovery is underway, and it appears the pandemic-induced recession – both globally and in the United States – is over, barring a severe virus resurgence. As for the U.S. economy, in September, the Fed revised its forecast sharply upward for the U.S. GDP this year to a 3.7% annual decline, compared to its June forecast of a 6.5% decline. The Fed is forecasting 4% U.S. real GDP growth in 2021, which is in line with consensus forecast.

A backdrop of rebounding U.S. and global economic growth should be supportive of equity and credit markets as increased consumer and business spending flows through to corporate sales and profits. But equity markets – large-cap U.S. stock valuations – are already assuming a continued recovery from the deep pandemic recession. So it remains to be seen how strong the actual recovery is and how much of it is already discounted in current prices.

The likelihood of an effective COVID-19 vaccine. Nine novel coronavirus vaccines are currently in phase 3 trials, including four candidates in the United States. Although far from a certainty, it seems a reasonable base case to assume there will be an effective and widely distributed vaccine within the next 12 months. This will be necessary for economic activity to return to its full pre-pandemic potential. In the meantime, countries, businesses, and communities are learning to adapt to living with the virus – via mask wearing, social distancing, digital rather than in-person meetings, better treatments – without total shutdowns of economic activity. We are confident this pandemic will end in the not-too-distant future. The financial markets seem to be pricing in a reasonably optimistic outlook on vaccine developments, so there is potential for short-term volatility and pullbacks if incremental news is disappointing. But there is also room for positive surprises on the medical side, and therefore in the stock market. As we have said all along, the current health crisis is deeply intertwined with the financial markets.

Extremely accommodative monetary policy. In response to the pandemic, the Fed pulled out all the stops, flooding markets with liquidity, purchasing government and corporate bonds, and cutting the federal funds rate to near zero. The Fed has made clear it remains committed to maximum monetary policy accommodation, given the state of the economy and uncertainty surrounding the pandemic.

At the September Federal Open Market Committee (FOMC) meeting, the vast majority of Fed officials indicated they do not expect to raise the fed funds interest rate at least through the end of 2023. Importantly, the Fed also introduced new “forward guidance” language, stating it would keep rates at zero until the labor market achieves “maximum employment” and inflation has risen to 2% and is on track to moderately exceed 2% for some time. This is the new policy of “average inflation targeting,” which you are certain to hear more about in coming quarters.

Other major central banks around the world have also been highly stimulative. Global central bank assets as a percentage of global GDP have spiked to an all-time high, an increase of nearly $7 trillion since the pandemic began. These central bank actions support financial asset markets and valuations. Additional fiscal stimulus, which seems likely whether before or after the U.S. election, would be further support.

The relative valuation of U.S. stocks versus bonds is attractive, and even more so for foreign stocks. Despite high absolute U.S. stock valuations, stocks look relatively cheap when compared to current sub-1% Treasury bond yields. The risk premium for owning equities relative to bonds is high and attractive, suggesting stocks should outperform bonds over a medium-term horizon.

With bonds and cash yielding little to nothing, investors seeking higher potential return, or yield, are pushed further out on the risk spectrum – for example, into equities and lower-credit-quality corporate bonds. This pushes stock prices and valuations higher. This has been the Fed’s explicit policy intent going back to the 2008 financial crisis. And as we note above, with the labor market far from full employment and inflation well below the Fed’s 2% average target, there is no end in sight to the Fed’s accommodative policies. Market downturns do happen while Fed policy is accommodative, but among many other considerations, weight must be given to the old market maxim “Don’t fight the Fed.”

Reasons for Caution

Balanced against the optimism noted above, we also see several reasons to remain cautious. The potential for market volatility and a stock market decline is elevated, primarily due to two unusual current events: (1) the U.S. election in November and (2) the ongoing coronavirus pandemic. No surprise there. Also of concern is the ever-present potential for a negative geopolitical shock. We will briefly address each of these below.

Election risk. For a variety of reasons, this election, and the circumstances surrounding it, really does seem unique. Absent a disputed election, the weeks leading up to Election Day are likely to be volatile. The fiscal and economic policy implications of a Trump versus Biden victory are meaningful, particularly if the Democrats sweep Congress. For example, a Democratic sweep, or Blue Wave, raises the likelihood of corporate and/or capital gains tax increases and market-unfriendly policies. On the other hand, the economy may get a near-term boost in a Biden administration from increased fiscal stimulus as well as the potential for a reduction in trade tensions and tariffs relative to a Trump administration.

This is certainly a monumental election along many dimensions. But from a long-term, fundamental investment perspective, we approach it as we have all past elections, including 2016’s. It is important not to let political views infect your investment process. While new facts and circumstances must always be incorporated into one’s fundamental investment analysis and decisions, election outcomes in any given year should rarely be the basis for major investment portfolio changes. Even more rarely should portfolio decisions be based on political predictions before the facts appear. History shows that the political party in power is not a significant differentiator or driver of investment returns. There are simply too many other factors, variables, and events that impact markets and asset prices over time, beyond election outcomes.

The economic risk due to a resurgence of COVID-19, along with potential lack of additional fiscal support. The coronavirus pandemic remains a significant risk facing financial markets in the near term. While the U.S. and global infection and death curves have been generally flattening/improving, the potential remains for a resurgence of COVID-19 in the fall and winter months. This raises the risk of renewed shutdowns and another economic downturn. Fed Chair Jerome Powell emphasized this at his September press conference, saying, “The outlook for the economy is extraordinarily uncertain and will depend in large part on our success in keeping the virus in check.” And he noted that “the overwhelming majority of private forecasters who project an ongoing recovery are assuming there will be a substantial additional fiscal support.”

However, as we share this market commentary, it remains unclear whether Republicans and Democrats will agree on another fiscal stimulus package. Time is running out, and the two sides still appear far apart in their negotiating positions. It would seem to be in everyone’s interest to agree on a new package. But if it does not happen, it could be a hit to fourth-quarter economic growth and likely the stock market as well. The extent of the impact will also depend on what is happening with the spread of COVID-19 and related medical developments.

Geopolitical risks and other unknowns. There is always the potential for a negative surprise or shock on the geopolitical stage. This is not meant to highlight any particular risk – although increasing U.S./China conflicts and the ongoing Brexit saga are two obvious ones – it is simply a reminder that stock markets and other “risk assets” are always subject to short-term volatility due to unexpected negative events and shocks. The coronavirus pandemic is only the most recent example. Although it can feel uncomfortable at the time, maintaining a disciplined, long-term investment approach through such periods is the best course of action. As we shared with you in March, these events often provide an excellent opportunity to invest in marked-down assets at attractive prices.

Current Portfolio Positioning

We are dealing with risks and unknowns on an unprecedented scale, with a wide range of possible outcomes. We will remain focused with both offense and defense in our portfolio construction. As always, we remain focused on meeting our clients’ longer-term financial goals and objectives, while managing and balancing nearer-term risks.

Maintaining broad diversification across multiple dimensions is very important, especially right now. In doing so, we believe our portfolios are positioned to provide solid returns on our base case, while still maintaining downside protection if a more challenging scenario plays out.

In our balanced accounts, we will focus on large-cap equities with strong balance sheets. In spite of the relative outperformance of U.S. large-cap equities, we see room for further appreciation, as these companies are in the best position to grow. We will look to add value or small-cap stocks opportunistically.

We are maintaining our positions in European stocks and emerging-market stocks because their expected returns look attractive. We will look to add to these positions, as foreign stocks offer attractive risk and reward characteristics. It’s also worth noting that in a scenario of sustained global economic recovery with Fed-repressed U.S. interest rates, odds are the U.S. dollar depreciates against foreign currencies and U.S. investors receive an additional positive currency return from holding international assets. Given the potential for higher returns and currency tailwind, we don’t want to reduce our global diversification right now.

We will look to add credit opportunistically to our fixed income when we see dislocation. Fixed-income yields are low, but we also do not see inflation as a near-term risk, given high unemployment and excess capacity.

Last, we will invest in real estate and infrastructure, as these investments generate solid cash flow at attractive prices.

Closing Thoughts: This Too Shall Pass

You’ve heard it from us before, but I will share it again: Investing requires discipline, patience, and a willingness to stand away from the herd at times. It can feel uncomfortable to stay the course – you might be nervous adding to equities when markets are plunging, or you might feel too uneasy to care about valuation and not chasing markets higher when they are soaring. But in the end, it is our belief that this is the best approach to achieving long-term returns.

Throughout history, the world has faced numerous challenges and economic downturns and has always come out the other side. While not minimizing the unique risks and unknowns of the current crisis, we will bet on that being the case again. 2020 is definitely testing everyone, yet our disciplined approach is keeping us focused on protecting and preserving your wealth, and we are grateful for the opportunity to serve you. Stay healthy!

Again, we are here and ready to do our best to answer any questions you may have or to just simply talk things through at times when you feel it may be helpful. We can navigate this current together; we are here for you.