Time to read: 7 minutes

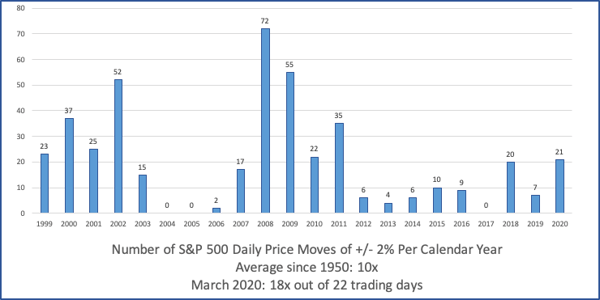

Today’s volatile investment environment has provided a moment for much needed self-reflection, particularly around one’s risk appetite. In the decade following the Great Financial Recession we saw many macro events which scared investors, but by and large, the past few years investors have been spoiled with strong equity returns with relatively low volatility. In 2017, per Standard & Poor’s, the S&P 500 had zero days where it moved plus-or-minus 2%. Historically, on average, that occurs around ten times in a calendar year. Just this past March, the S&P 500 saw 18 of its 22 trading days move at least 2% in either direction!

Given the magnitude of the recent volatility, many investors want to take action for action’s sake. It can definitely make people feel better. But oftentimes in investing, that’s exactly the wrong thing to do. Trying to time market tops and bottoms is a zero sum game. “The bottom” is technically the day before the recovery begins and it’s impossible to know exactly when the bottom hit until months or even years later. The evidence is overwhelming that most investors diminish their long-term returns trying to do so. They are more likely to chase the market up and down, and get whipsawed, buying high and selling low. Market timing, while tempting, involves getting two nearly impossible decisions right: when to sell and when to get back in.

Missing the Worst Days … Means Missing the Best Days

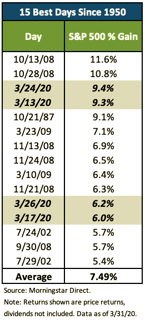

Bear markets provide opportunities for long-term investors. There’s a reason why one of Warren Buffett’s most famous quotes is, “Be fearful when others are greedy, and be greedy only when others are fearful.” The table to the right shows that the 15 best days for the S&P 500 all occurred within bear markets, not bull markets as one might expect. That is, the times when it’s hardest to remain invested or tempting to get out of the market and wait for better days. Looking at these dates, you’ll see “end of days” events such as: the Great Financial Recession, the Tech Wreck, the Black Monday crash of 1987 ... and COVID-19.

By trying to miss the worst days, investors are very likely to miss the best days. “Recency bias” suggests that someone’s most recent experience has the greatest influence on their decisions. As such, investors tend to sell after a meaningful market selloff and buy after a market rally.

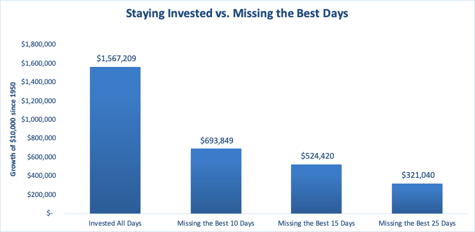

Missing just the 10 best days (out of more than 17,500 trading days since 1950) has a huge long-term effect on a portfolio. For example, an investor who invested $10,000 in the S&P 500 in 1950 would have gained 7.5% annualized and finished with a portfolio value of more than $1.5 million (as of 3/31/2020) if they had remained fully invested (not including dividends). The final portfolio value for an investor that missed the 10 best days is much, much lower—just shy of $700,000.

Now it is unlikely an investor will only miss the best days if they attempt to time the market. They might also be able to miss some of the historically bad days. However, the cautionary tale of attempting to time the market is the same: There can be a huge cost to pay if the market swings to the upside while you’re on the sidelines. It would take exceptional timing skills to get in and out of the market perfectly, particularly since it needs to be done in short order given the market’s best and worst days tend to cluster close to one another. Staying the course is the best plan of action during periods of severe market stress. There is an old investing adage: “Time in the market beats timing the market.”

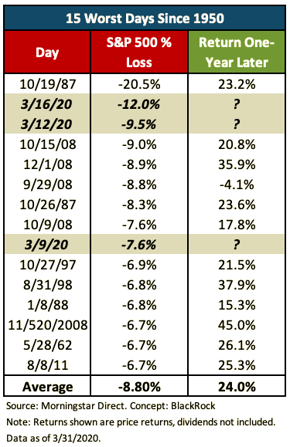

Owning stocks on historically bad days can be unsettling, but outcomes over the next year tend to be favorable. BlackRock recently published a table showing one-year returns following the worst days for the S&P 500. The average one-year return after a historically bad day has been 24%. And there has only been one instance of a negative return.

Staying Invested, Staying Resilient, Being Agile

Part of our job as your wealth advisor is to help you stay the course and stay true to your long-term investment strategy guidelines to better achieve your long-term goals. We don’t want to sell out of the equities you already own during this downturn, only to try to decide when to jump back in so we catch the rebound. On the contrary, we want to stay invested, which we believe is the only sure-fire way to capture a recovery in prices. What’s more, we will want to be agile and prudently add incrementally to equity allocations depending on your investment strategy guidelines as forward-looking returns look more and more attractive. For new cash, this may include dollar cost averaging which can reduce the effects of volatility by stretching asset purchases over time. With this strategy we hope to catch some of the best prices in this market cycle. The potential higher returns should bolster your financial situation in the years to come.

Again, we are here and ready to do our best to answer any questions you may have or to just simply talk things through at times when you feel it may be helpful. We can navigate this current together; we are here for you.