12 minute read

After a record-setting year in 2021 for the markets, we saw the return of volatility to start 2022. In fact, volatility returned with a vengeance in the first quarter of 2022, which has been more volatile than all of 2021. Indeed, it is true that the stock market had “everything but the kitchen sink” thrown at it in the past quarter, including a surge in inflation to 40-year highs, the Federal Reserve’s promise to raise rates faster than expected, and Russia surprising the world with a full-scale military invasion of Ukraine, marking the first major conflict in Europe in decades. All of these factors contributed to market turbulence in the first quarter.

With so much turbulence all at once, it is no surprise that financial markets had a rough quarter across the board – stocks, bonds, U.S., international, and emerging markets (EMs). Global stocks (MSCI ACWI Index) fell 5.4% for the quarter. Among major global markets, the S&P 500 was a relative outperformer, dropping only 4.6%, compared with developed international markets (MSCI EAFE Index) down 5.9% and EM stocks down 7.0%.

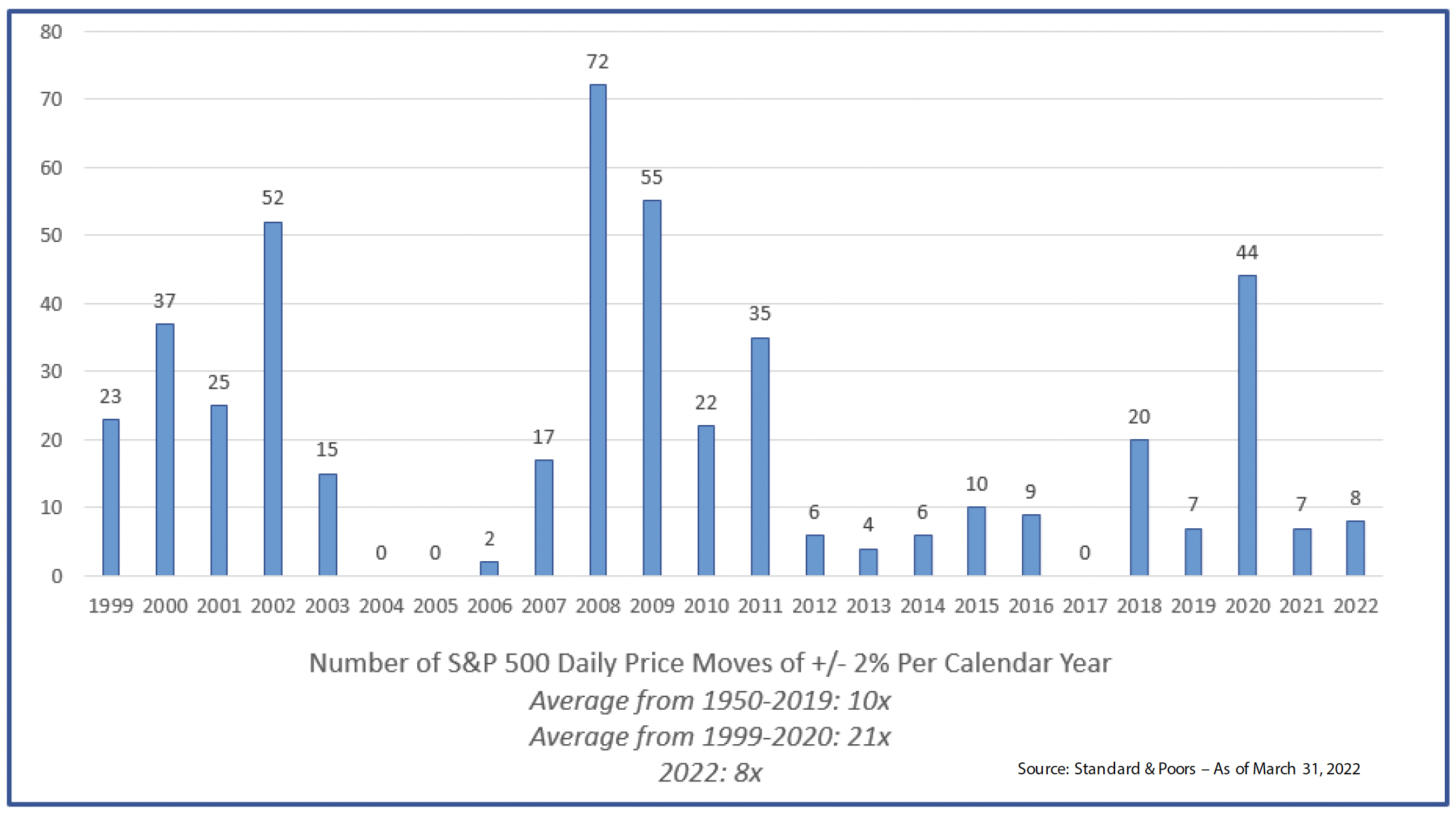

The relatively mild declines for the full quarter masked the intra-quarter volatility. But as an investor you know this, as you had to stomach some wild swings throughout the quarter. To help put that in context, here are some data points. At its low point on March 8, the S&P 500 was down 13% from its high on January 3. The developed international and EM stock indexes had drawdowns in the 16-17% range during the quarter, before rebounding roughly 10% from the lows by quarter-end.

Unusually, the damage was worse in the U.S. core bond market than in the U.S. stock market. The Bloomberg U.S. Aggregate Bond Index (the Agg) fell 5.9% for the quarter. This was the second-worst quarter for the Agg since Q1 of 1980, when the Fed was in full-bore tightening mode.

As we’ve discussed, a period of rising inflation and rising interest rates creates challenges for both bonds and stocks and, in turn, for a traditional balanced portfolio comprised only of core bonds and stocks. Diversification into other asset classes, market segments, and alternative strategies can particularly be valuable in such an environment. Real estate, commodities, and alternative strategies have added value to our diversified portfolios. In the fixed income markets outside of core bonds, credit strategies and floating-rate loans have declined less than core bonds. Private real estate investments performed well for the quarter as they are driven by rent rates, which increased much higher than expected. There never being any guaranty that these areas will continue to perform well, based upon current conditions, we remain confident that our investment approach, with our focus on risk control and a strict valuation discipline, will lead us to opportunities which will serve our clients well over the long term.

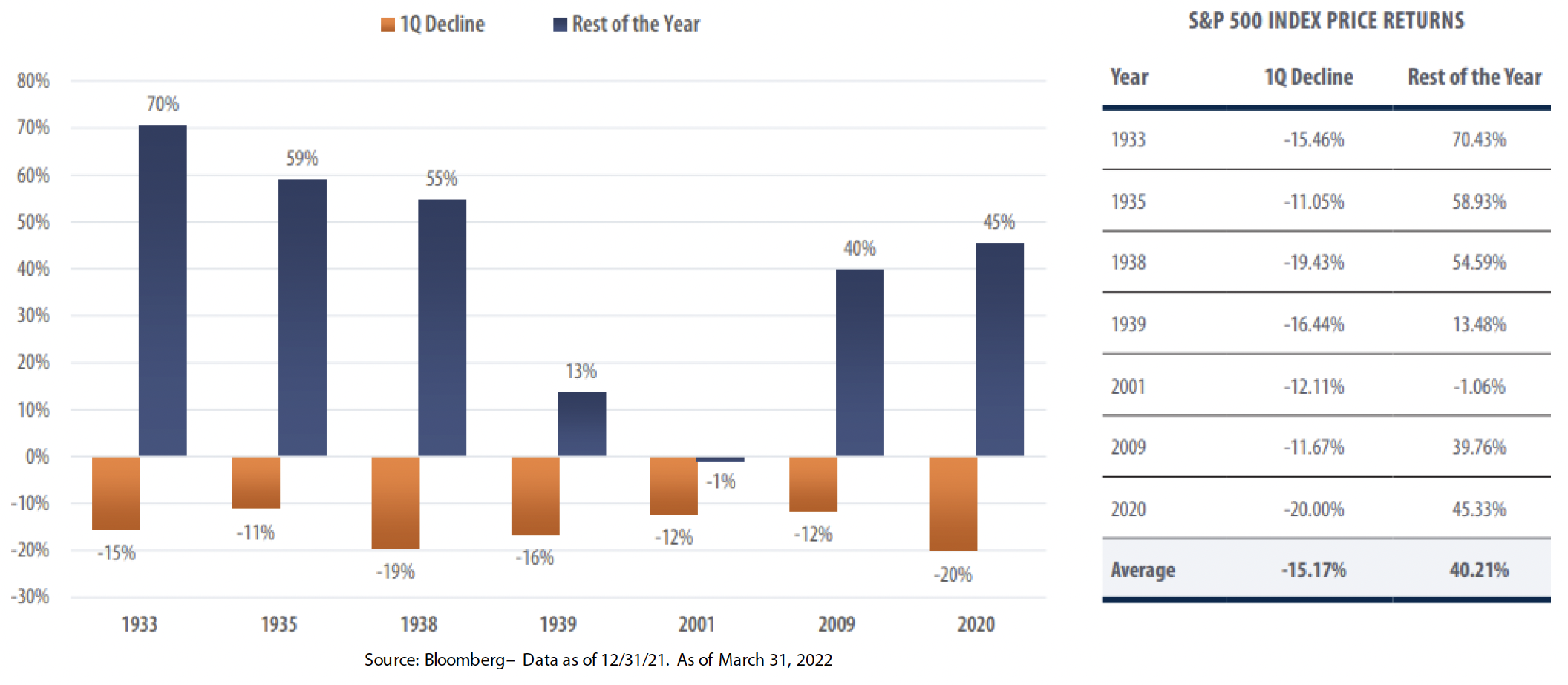

After a down quarter for the market, it is natural to wonder what is in store for the rest of the year. And sometimes the first 90 days of the year are a good proxy for what it is to come. Although it is impossible to predict what will happen, we can look at data from previous down first quarters to see what has happened. From 1928-2021, there were seven first quarters with a decline of greater than 10%. In six of seven instances, the rest of the year provided a positive return.

Like any data point, it is interesting to study and see what could be a range of possible outcomes. But with so much noise in the macro environment, we are not holding our breath.

Macro Backdrop: We Remain Cautiously Optimistic, but Inflation and Recession Risks Have Risen

The war in Ukraine has had wide-ranging but diverse impacts on the global economy and individual regions. The most direct and damaging economic impact has been on not only Ukraine but also Russia. Given that Russia’s economy is less than 2% of global GDP and that our portfolios had close to zero exposure to Russian stocks or bonds, the economic impact on the Russian economy in and of itself does not concern us – it is essentially immaterial to our investment strategy

However, Russia is a major producer and exporter of oil and natural gas – to Europe in particular, accounting for roughly 50% of Europe’s natural gas imports and 25% of its oil imports – and certain agricultural commodities and base metals. As such, the war and the sanctions imposed on Russia by the West are having, and for the foreseeable future will continue to have, a material impact on global economic growth and inflation.

In a nutshell, the war is a “stagflationary” supply shock: It fuels higher inflation via sharply rising commodity prices (especially oil) while also depressing growth via negative impacts on real disposable income and consumer spending. It is also triggering various government and central bank policy responses that, as we discuss below, create additional risks and uncertainties for the economy and markets, given already-high inflation and decelerating growth coming into the year.

As we write this, the path, timing, impact, and ultimate outcome of the war are highly uncertain. Russian and Ukrainian commodity exports could be further disrupted, forcing prices even higher; the conflict with Russia could expand beyond Ukraine, with even more death and destruction. On the other hand, we may be positively surprised by a quick and/or less destructive resolution than the current consensus would indicate. As we’ve often said about shocking events such as this, the truth is, no one knows.

As such, we continue to frame our macro outlook and market analysis by incorporating a range of scenarios and outcomes we believe are plausible. We strive to construct our client portfolios to be balanced, diversified, and resilient across this range. We also proceed with a large dose of humility. The future is inherently uncertain. We should be prepared to expect the unexpected. In short, we want to build portfolios that are resilient in the face of surprises rather than ones whose success depends on predicting them.

Economic Conditions: Growth and Inflation

With the war in Ukraine, most economists and strategists have lowered their 2022 economic growth forecasts and upped their inflation forecasts, reflecting the expected stagflationary impacts discussed above.

On the growth side, for example, global GDP growth forecasts have been cut from around 4% to 3% for the year, which is only slightly above the economy’s long-term trend growth rate. The Federal Reserve, at its March FOMC meeting, cut its 2022 U.S. real GDP growth forecast from 4% to 2.8%.

Growth forecasts for Europe have taken the biggest hit since the war. For example, Ned Davis Research (NDR) cut its 2022 Europe real GDP forecast from 4% to 2.7%. Oil prices are up more than 30% this year to around $100 per barrel, while European natural gas prices have soared nearly 80%. NDR estimates that a $20 increase in real (inflation-adjusted) oil prices would shave .6 percentage points off European GDP growth. However, absent a significant escalation in the war, NDR still sees a low risk of recession in Europe this year due to large household savings, pent-up consumer demand from the pandemic, a strong job market (eurozone unemployment recently hit a record low at 6.8%), and additional fiscal stimulus on the way.

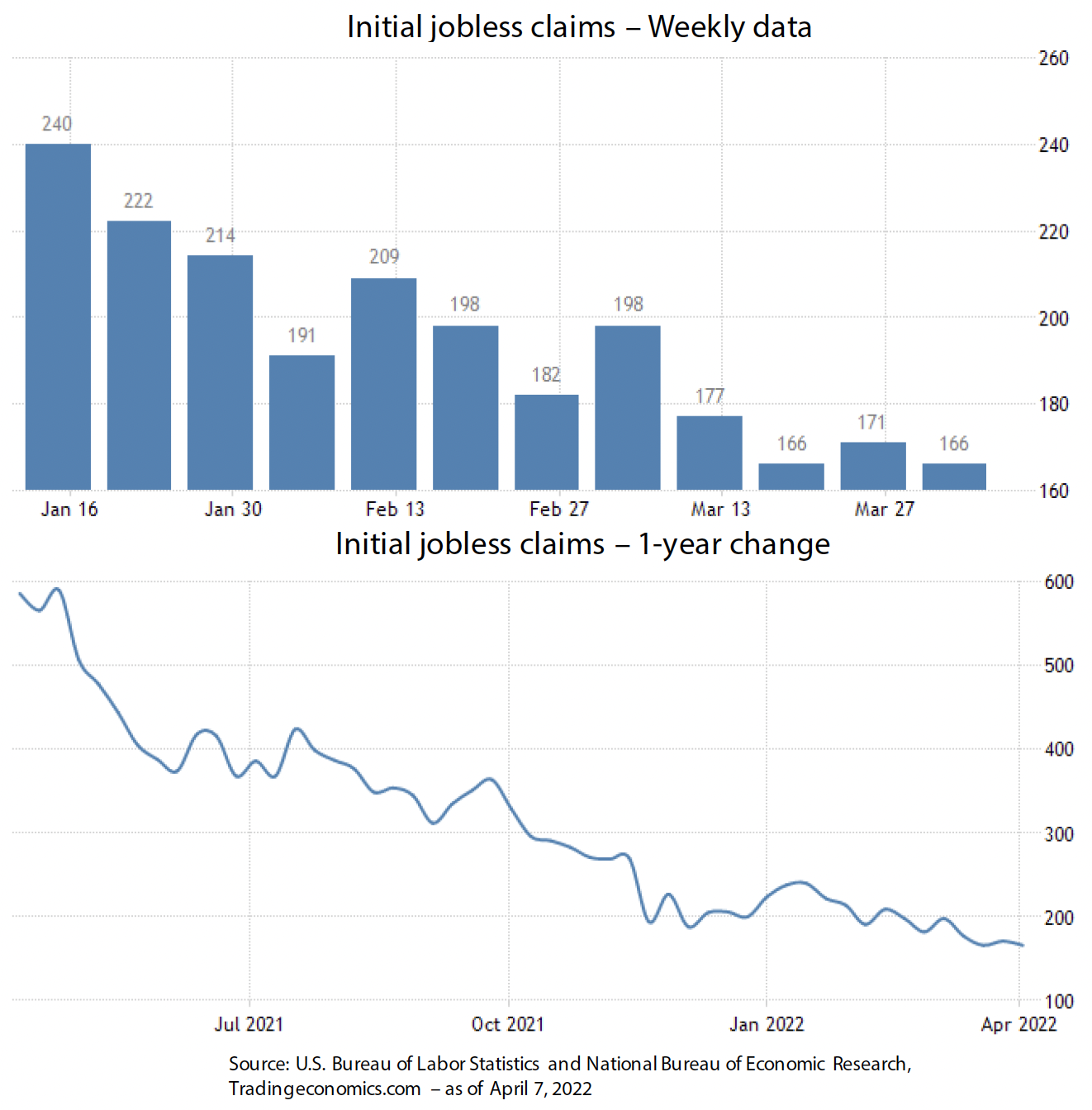

Most of the evidence also suggests that a U.S. recession in the next 12 months is unlikely. Several recent U.S. economic data points have been solid/strong, including expansionary Purchasing Manager Index (PMI) readings, record-high job openings, record-low weekly new unemployment claims, and a positive Leading Economic Indicator (LEI).

Household wealth and savings are also high, which should support consumer borrowing and spending even with high inflation and rising interest rates. Corporate balance sheets are also generally in good shape. The economy is less sensitive to oil price spikes and much less exposed than during the 1970s OPEC oil crisis. The U.S. is also now a slight net exporter of petroleum, which mitigates the overall economic damage from rising oil prices, although domestic consumers – lower-income households in particular – usually suffer. These are all very positive signs. As things currently stand, the U.S. and global economies still look likely to post solid growth this year, albeit lower than was expected three months ago.

Moving on to the inflation backdrop in the U.S., the news has unfortunately gotten worse over the past three months, as can be seen across any number of inflation measures: core, median, and trimmed mean. The highest inflation by far is still coming from the consumer goods side of the economy, where the supply/demand imbalances due to COVID (and now the conflict in Ukraine) are worst. These imbalances should recede as the pandemic recedes, reducing at least some of the broad inflationary pressure. While most forecasters expect U.S. inflation to be lower by year-end than it is now, the consensus estimate has risen compared with three months ago. This includes the Fed. At its March FOMC meeting, it projected core PCE inflation of 4.1% for this year, up from its 2.7% forecast last December. The persistence of high and broadening inflation has led to a further hawkish shift in the Fed’s monetary policy stance.

Monetary and Fiscal Policy

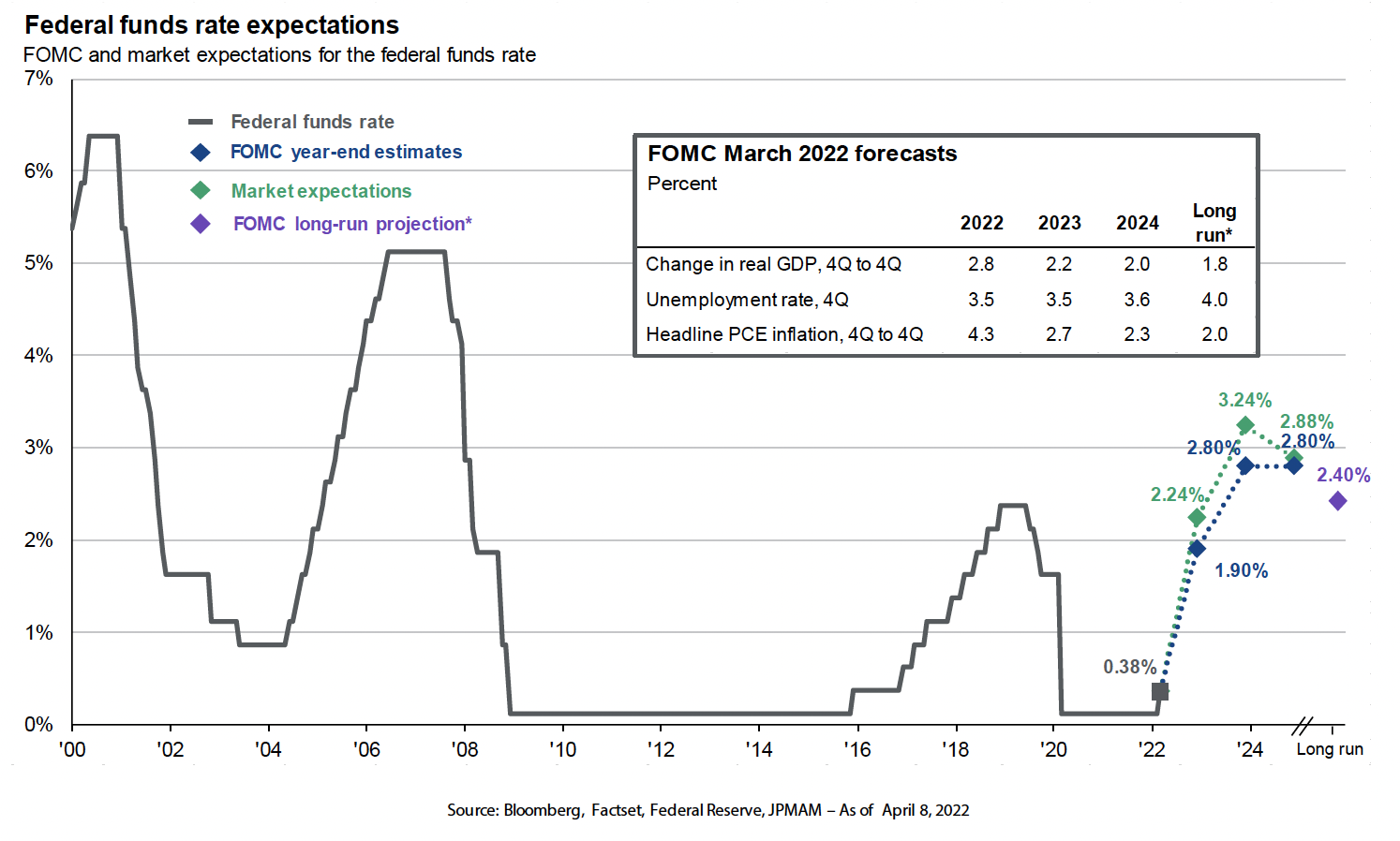

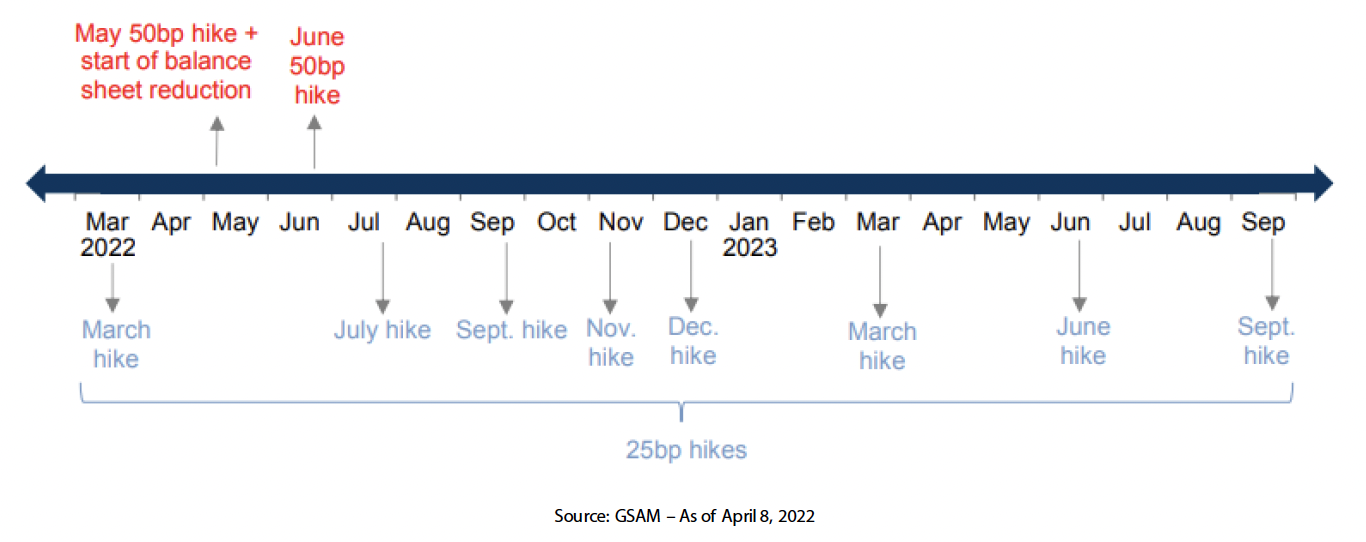

The Fed has finally begun to raise interest rates (the Fed funds policy rate), starting with a 25-basis-point increase at the March FOMC meeting. The chart shows the sharp increase in the Fed funds rate the FOMC now expects in 2022 and 2023 compared with its previous meeting in December: 1.9% (2022) and 2.8% (2023) vs .9% and 1.6%, respectively.

The Fed also indicated it will start to shrink its $9 trillion balance sheet of Treasury and government agency mortgage-backed securities this year. This is another form of monetary tightening – quantitative tightening (QT), the opposite of quantitative easing (QE)

In his post–FOMC meeting comments, Fed Chair Powell clearly stated that fighting inflation is the Fed’s focus, now that the labor market has reached maximum employment and then some. On the more positive side, longer-term inflation expectations remain mostly anchored in a range consistent with the Fed’s 2% long-term core inflation target. Short-term (12-month) inflation expectations have spiked higher, consistent with the recent sharp rise in gasoline prices and overall CPI. Should longer-term expectations move higher, we’d expect the Fed to accelerate its tightening pace.

Powell and the Fed are in a tough spot. They know they need to tighten to combat high inflation, keep longer-term inflation expectations anchored, and prevent a wage-price spiral from taking hold. If they fail, it will require even more drastic policy tightening down the road. Yet much of the current inflation is driven by exogenous supply-side disruptions due to COVID and the Ukrainian war, which the Fed can’t control. Raising rates is intended to crimp aggregate demand, i.e., consumer and business spending. This should eventually have a downward impact on inflation. But it also raises the risk of driving the economy into a recession or near recession and increasing unemployment.

In terms of monetary policy outside the U.S., roughly two-thirds of global central banks have also been raising interest rates. The notable exceptions continue to be the European Central Bank and the Bank of Japan. China is also a notable outlier as it has started cutting rates and increasing fiscal spending to stimulate its economy.

In our 2021 year-end commentary, after unprecedented stimulus in 2020 and 2021, both fiscal and monetary policy in the U.S. were set to tighten in 2022. There hasn’t been any major change on the fiscal side. Meaningful new stimulus appears unlikely. Instead, the economy faces a fiscal growth drag, estimated to be in the range of negative to 2-3% this year.

Economic Outlook

Our base case shorter-term (12-month) economic outlook is for decelerating economic growth and still high, but moderating, inflation. Absent a recession, which of course we can’t totally rule out, this macroeconomic backdrop should be generally supportive for “risk asset” returns, such as global equity and credit markets, and a headwind for core bonds in the face of rising government bond yields.

We’ve seen the latter play out so far this year, with sharply negative bond returns. Risk asset markets have also been generally negative, but not much worse than core bonds and in some cases better. As we’ll discuss in the next section, we believe equity and credit have relatively attractive return potential from current levels.

Our view of the key risks around our base case are as follows:

- The war in Ukraine intensifies, causing deeper economic damage.

- A new highly infectious and deadly COVID variant emerges, leading to renewed lockdowns.

- The Fed makes a policy mistake – either tightens too much, causing a recession, or allows an inflation spiral to take hold.

- The Chinese economy has a sharp downturn due to a policy mistake.

- Another geopolitical or exogenous shock impacts the global economy.

We will be watching closely as the various scenarios play out, and we will make adjustments as necessary. Our job as long-term investors is to sift through the shorter-term market noise, stand back from the emotional whipsaw of the day-to-day headlines, and remain focused on the interplay between underlying economic fundamentals and the financial markets’ current pricing. In other words, “What’s in the price?” When we gain conviction that the current market pricing is significantly out of whack with our view of the fundamentals, we will tactically reposition our portfolios. Otherwise, we stay the course, confident that our portfolios have a well-diversified balance of defensive assets that are able to withstand shorter-–term negative outcomes or shocks and riskier “offensive” assets that are the primary long-term return generators and wealth builders. We try to build “all-weather” portfolios.

This is a long way of saying that we plan on making some modest portfolio changes. The war in Ukraine has increased the upside inflation risk and downside growth risk. As a result, we plan on modestly reducing our U.S. equities from a maximum overweight to a slight overweight and redeploying those assets into our alternative strategies, which provide diversification and better upside than does fixed income. We continue to favor equities over fixed Income.

Portfolio Positioning

We believe the portfolios are well positioned to generate relatively solid returns in our most likely baseline scenario of continued global growth with rising interest rates and inflation and decelerating growth in the U.S. But our balanced portfolios should also prove resilient if we have an inflation or growth scare.

In terms of our overall risk exposure in our globally diversified moderate portfolios, we are overweighting equities relative to bonds. The relative valuation of U.S. stocks versus bonds is attractive, and even more so for foreign stocks. Despite high absolute U.S. stock valuations, stocks look relatively cheap at a 5% earnings yield when compared with a 2.5% Treasury bond. We also see tactical opportunities in foreign stocks as we are being fairly compensated for investing in these markets over the next five years.

We believe Treasury rates will be pressured higher from current levels due to global growth and higher-than-expected inflation. As a result, we favor short-term credit strategies over core bonds. We have a bias toward reflationary assets, and in our alternative investments we own real estate, infrastructure, and commodities as portfolio diversifiers and risk reducers that we expect will do better if inflation rises or stays higher longer.

Closing Thoughts

There were a lot of different ways the start of 2022 could have gone, but the current scenario is one very few would have predicted. The war in Ukraine has added to the already-high uncertainty, reduced the near-term growth outlook, and added fuel to the inflationary fire. It is true that crises often create opportunities. However, the equity and fixed income markets have reacted quickly to the headlines, and as they are currently priced, they aren’t offering any compelling new opportunities in our view.

Our balanced portfolios remain positioned with the following attributes:

- a slight overweight to global equities, coming from our tactical overweight to U.S. Large equities and modest overweight to EM equities;

- a large underweight to core bonds, but a still-meaningful allocation to bonds; and

- core positions in alternative investments like real estate, infrastructure, and commodities.

In many of our client accounts, we also have core holdings in private real estate, private credit, and private equity. We believe these investments offer attractive long-term return potential plus additional portfolio diversification benefits, though with less liquidity, relative to publicly traded securities

While tilting toward our highest-conviction tactical views, our portfolios remain strategically balanced and well diversified across multiple global asset classes, investment strategies, and equity styles. This should enable them to be resilient should a risk scenario or shock outside our cautiously optimistic base case occur.

We are confident that our long-term, team-driven investment process, research depth and discipline, and access to exceptional managers will enable us to continue to navigate whatever macro and market environments come our way. As investors, we always need to be prepared for the worst, even as we hope for the best. But it is not “hope” that will get us through this volatility. It is having a disciplined, research-driven investment process, and we are following that approach closely as we encounter an unprecedented amount of change in the macro environment. We sincerely appreciate your confidence and trust in us.

Register for our upcoming webinar on Wednesday, May 18 at noon PT to hear our thoughts on this commentary and more on what to expect in the coming months.