5 minute read

Smart insight and clear visuals that matter – what we’re watching now and how intention and conviction shape our portfolios.

Markets

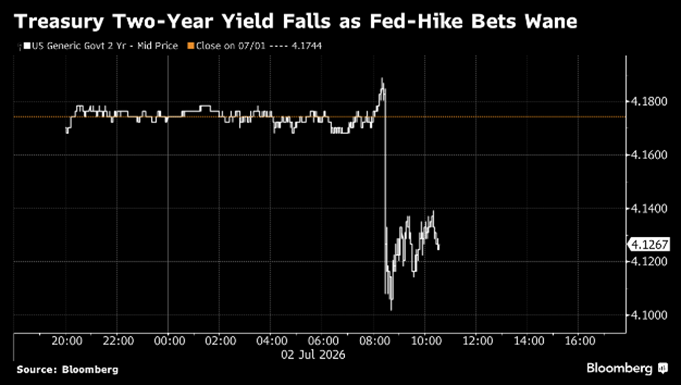

A slower than anticipated increase in US jobs drove most stocks higher as short-dated bond yields fell on bets the Federal Reserve won’t be forced to raise interest rates.

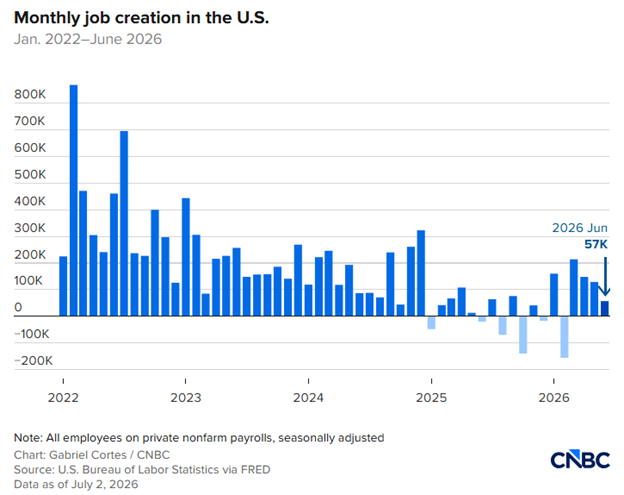

- Nonfarm payrolls for June increased by 57,000 in June, slower than the downwardly revised 129,000 added in May and worse than the 115,000 Dow Jones consensus forecast. (Supported by Chart A)

- The unemployment rate, however, dropped to 4.2%, largely due to a slump in the labor force participation rate, which fell 0.3 percentage point to 61.5%, the lowest since March 2021.

- Household employment plummeted during the month, with 507,000 fewer people reported at work. (Source: Jobs Report June 2026, CNBC, July 2, 2026)

Chart A

Chart B

Tech

AI and Memory Trade

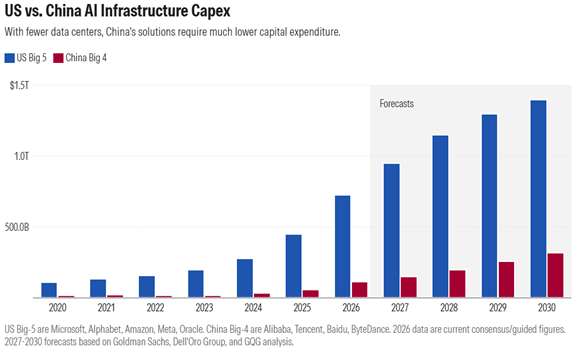

The center of the AI trade in 2026 has been memory. Whether you believe AI is still in the early innings or that it is a bubble about to burst, memory fits both arguments. While market attention often fixates on daily price movements, we believe the underlying technology requires continuous physical upgrades. As AI models evolve from simple chatbots that answer isolated questions into sophisticated digital assistants capable of executing multi-step processes, the infrastructure supporting them must expand. These advanced systems require more than just raw processing power; they need robust memory architecture to retain context, compare alternatives, and retrieve data efficiently. When considering that a single enterprise might eventually run thousands of these automated workflows simultaneously, the compounding demand for physical data storage becomes clear.

Currently, there appears to be no immediate signs of a slowdown in infrastructure spending. However, the primary risk on the horizon centers on return on investment. If the market begins to doubt whether major cloud providers and leading AI developers can successfully monetize these heavy capital expenditures, the willingness to fund future projects could stall quickly. This vulnerability could be further amplified by the highly interconnected financial relationships within the industry—such as hardware manufacturers taking equity stakes in the very software companies purchasing their chips.

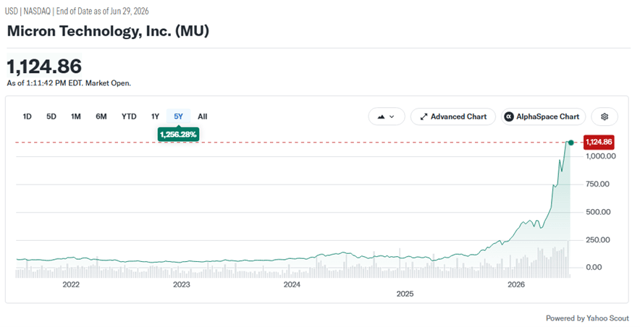

As AI models become more sophisticated, memory increasingly serves as a bottleneck rather than a commodity. This dynamic has elevated memory manufacturers such as Micron to a central position within the AI supply chain, helping explain the outsized stock performance shown in Chart C.

Chart C

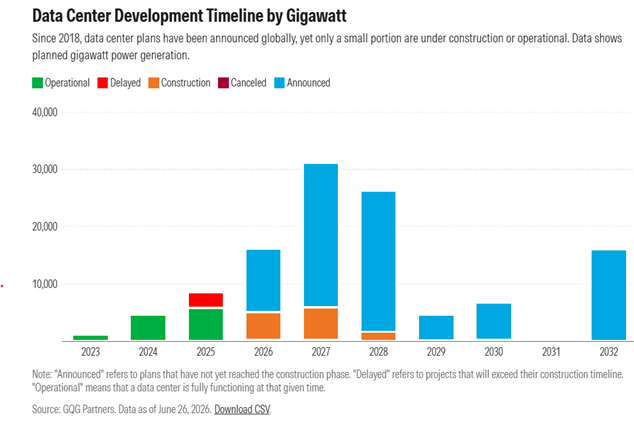

Further elaborating on the question, will the large AI build out result in attractive return on investment? The market is asking, will the massive AI capex cycle produce enough incremental revenue, margin expansion, and defensible productivity gains to justify the spending. Skeptics point to the risk of cheaper alternatives and potential signs of delay in data center development.

- Developers are increasingly using open-source models from China that are cheaper to train and come with significantly lower infrastructure capex. If businesses prefer SLMs (or small language models that perform specific business tasks with fewer parameters and lower computing requirements) for their solutions, the fund manager GQG believes “the broader implication is that the market may not need nearly as much frontier-scale compute as investors currently assume”. (Source: Morningstar, June 26, 2026)

- Then there are the uncertainties around the ability to build the data centers currently ordered. Backlash against data center infrastructure is growing due to heavy use of electricity and water, as well as their other impacts on communities.

- GQG estimate “roughly half that were supposed to be completed haven’t even started or were cancelled” (Source: Morningstar, June 26, 2026)

- Meta's announcement that it plans to sell compute capacity unsettled the market last week, as investors grew concerned that increased supply could lead to an oversupply of compute resources. (Source: Reuters, July 1, 2026)

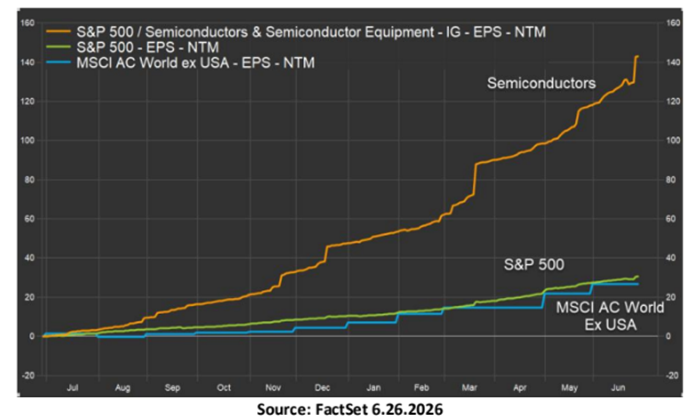

In the meantime, Chart F below shows next twelve months (NTM) earnings per share (EPS) for the S&P 500 semiconductor industry, the S&P 500, and MSCI ACWI ex-USA.

- Semiconductor earnings revisions remain exceptionally strong, reflecting pricing dynamics that resemble a near “sold-out” market.

Rates

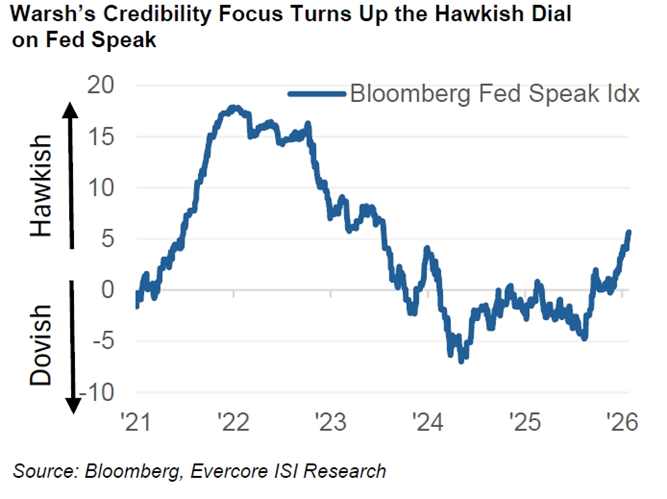

Federal Reserve Chair Kevin Warsh has so far struck a hawkish, credibility-first tone rather than signaling a willingness to let the economy run hot. Given the Fed’s strict focus on returning inflation to 2% (Source CNBC, July 1, 2026), market consensus is building toward at least one rate hike before the end of the year. Some institutions are taking an even firmer stance: both PGIM and Bank of America are now forecasting up to three increases—a notable shift from their earlier projections in the first quarter.

Public REITs

Public REITs are aggressively expanding into the digital infrastructure market to capitalize on AI and cloud computing.

- On 6/30, Realty Income committed up to $1.4 billion for a 45% equity stake in a Northern Virginia data center venture, which anchors a broader portfolio of hyperscale assets valued at over $6 billion.

- The assets are underpinned by 15-year to 20-year triple net lease agreements with investment‑grade hyperscale tenants, featuring embedded annual rent. (Source: Realty Income, June 30, 2026)

- On 6/29, Digital Realty agreed to purchase Blackstone’s 80% interest in two 96 megawatt data centers in Manassas, Virginia and a 50% interest in one 96 megawatt data center in Sterling, Virginia for $3.5 billion

- At a gross value of $7.8 billion, reflecting an expected initial stabilized capitalization rate of over 6.5%.

- 100% leased to three distinct investment grade hyperscale customers supported by 15-year leases and 3.6% annual rent escalators. (Source: Digital Reality, June 29, 2026)

In the first quarter, Prologis started $1.3 billion of data center build-to-suit projects. (Source: Prologis Reports, April 16, 2026)

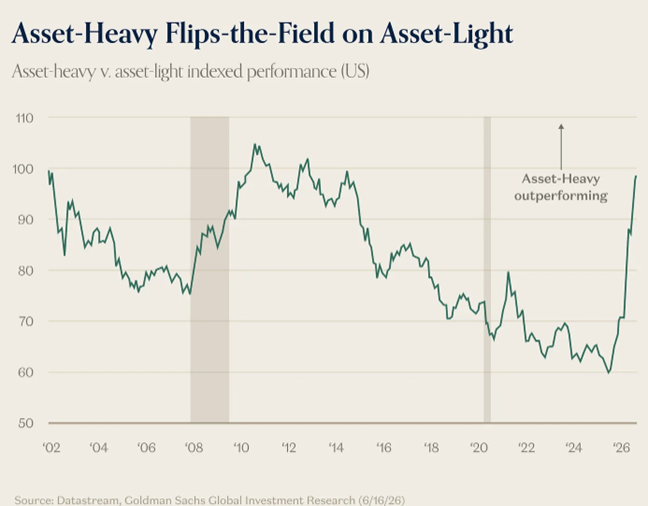

Sectors

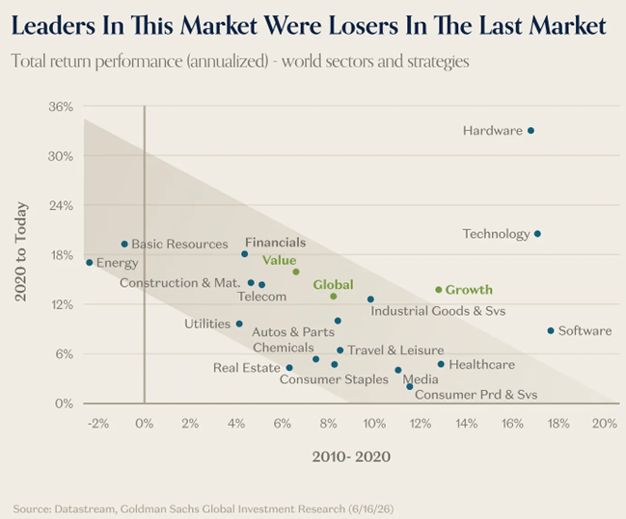

If you compare this cycle to the previous one, in some ways it’s exactly the same, and in other ways, it’s a complete inversion.

- Tech has been the cycle winner for both the post GFC period (2010-20) and the post-pandemic period (2020-present). The rest of the field, however, has flipped the last cycle’s winners are now losers, and vice versa

- Markets have shifted their attention from capital-light, consumer-oriented sectors, and now cast their loving eyes on the capital-heavy “real” economy, driven in large part by the AI infra buildout.

-

- Healthcare, consumer products and media all offered double-digit returns post-GFC but are now doing mid-single digits returns.

- Energy, raw materials, construction and financials all went from low single-digits to mid-to-high double-digits.

Economic Calendar: Week Ahead (Eastern Time)

Mon, 7/6 @ 9:45 am: U.S. Services PMI

@ 10:00 am: ISM Report On Business Services PMI

@ 11:00 am: Global Services PMI

Wed, 7/8 @ 10:00 am: Monthly Wholesale Trade

@ 2:00 pm: FOMC Meeting Minutes and Economic Forecast

@ 3:00 pm: Consumer Credit

Thur, 7/9 @ 8:30 am: Weekly Jobless Claims

@ 10:00 am: Existing Home Sales

The Team Behind Friday Focus

Mary Ahn

Investment Research and Portfolio Strategy Manager

Cal Jones, CFA

Managing Director of Fixed Income

Eric Speron, CFA

Managing Director of Equities

Alton Tjahyono, CFA

Sr. Investment Strategist