6 minute read

Smart insight and clear visuals that matter – what we’re watching now and how intention and conviction shape our portfolios.

The Fed and Inflation

Markets are repositioning following the latest inflation report. Headline CPI reaccelerated to 4.2% year-over-year in May, up from 3.8% in April (Source: BLS; Bloomberg, June 2026). While this headline figure landed in line with consensus estimates, the underlying data highlights a complex policy challenge. The primary catalyst for the advance was a sharp 23.5% year-over-year increase in the energy index—marking the highest level of energy inflation observed since August 2022 (Source: BLS).

This latest data point underscores an ongoing, structural reality: the U.S. economy has now operated above the Federal Reserve’s official 2% target for more than five years. The consistency of these above-target prints leave the central bank with a narrowing margin for error as it attempts to balance price stability against broader economic growth.

Source: Bloomberg

IPO Summer

Last Friday marked a watershed moment for capital markets as SPCX executed the largest initial public offering in history. Pricing a $75 billion block of stock at $135 per share, the deal pegged the company's implied valuation at $1.75 trillion (Source: Reuters, June 11, 2026). The market’s appetite was both immediate and voracious, with investors rewarding the debut and sending the stock up nearly 19% from the open to the closing bell. (Source: TechCrunch; CNBC, June 12, 2026)

This entry aligns with historical patterns for highly anticipated public debuts. Across the broader universe of IPOs, the opening "pop" is a consistent phenomenon:

-

First-Day Consistency: Newly issued shares land in the green roughly 81% of the time on their opening day

-

Outsized Returns: The median Day-1 gain hovers around an impressive 33.6% (Source: Bloomberg, Evercore ISI Research)

Looking past the opening-day fanfare, however, history suggests a healthy dose of caution is warranted. Over longer holding periods, performance tends to reveal a more bifurcated landscape. By year-end, the initial excitement fades, often separating newly public companies into “winners” and “laggards” rather than settling into modest, average gains. This leaves durable portfolio performance to be determined by whether the underlying business fundamentals will justify the price tag.

Employment

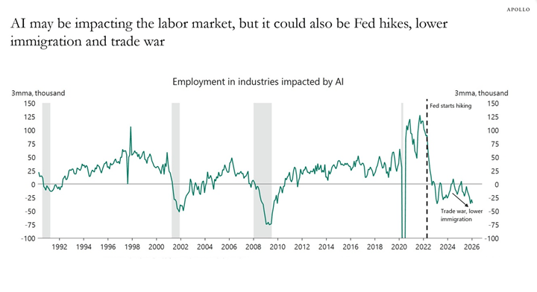

Recent employment weakness in AI‑exposed industries is likely being overattributed to AI alone. While generative AI adoption has accelerated since late 2022 (see chart below), the downturn in hiring across these sectors coincides closely with a broader set of macro shocks—including aggressive Fed tightening, elevated trade uncertainty, and a slowdown in immigration-driven labor supply. Given that many AI-exposed sectors are also highly sensitive to interest rates, global trade, and talent flows, the labor market softening is best understood as a confluence of these forces rather than a pure reflection of AI-driven displacement.

- Timing matters: The inflection in employment aligns more closely with the start of Fed rate hikes than with AI adoption cycles.

- Macro overlap: AI-exposed sectors (tech, finance, professional services) are disproportionately sensitive to rates and investment cycles.

- Trade and geopolitics: Ongoing trade frictions have weighed on globally integrated industries.

Labor supply dynamics: Slower immigration has constrained hiring, particularly in high-skill segments where AI exposure is highest.

Source: US Bureau of Labor Statistics (BLS), Macrobond, Apollo Chief Economist

The World Portfolio

The “World Portfolio” is simply a theoretical snapshot of all investable assets globally—across equities, bonds, real estate, private markets, gold and other alternatives—weighted by their market size. In other words, it shows how the global investment universe is currently distributed and, by extension, how a fully passive investor would be allocated if they owned “everything.” While this makes it an interesting reference point for understanding broad market structure and trends, it is not designed to be an optimal portfolio. Because it is market-cap weighted, it naturally becomes concentrated in whatever has performed best (currently US equities and bonds), and it implicitly assumes those trends will persist—embedding strong views on future returns, valuations and currency dynamics.

Goldman Sachs highlights that investors should be cautious about using this framework as a blueprint for portfolio construction and instead treat it as a starting point for more active allocation decisions.

- Concentration risk: Today’s global weights are heavily skewed toward US assets, implying continued outperformance that may be difficult to sustain given elevated valuations and potential FX headwinds.

-

Missed diversification: A pure “world portfolio” approach underweights smaller asset classes and alternatives, which can improve risk-adjusted returns when incorporated thoughtfully.

Source: Goldman Sachs Research

Since the 1990s, the World Portfolio has grown from 75% to over 200% of world GDP.

Private Equity

Bain’s highly regarded mid-year 2026 Global Private Equity Report offers a sobering look under the hood of the current alternatives landscape. One of the standout metrics is the firm's "deal cost index," which aggregates purchase multiples and debt financing costs to confirm what many dealmakers already feel: buyouts are currently as expensive as they have ever been. The takeaway seems absolute. The era of relying on cheap leverage and multiple expansion to generate returns is over, meaning future alpha must be engineered through genuine operational improvements at the company level. Furthermore, forward-looking data suggests this sluggish environment will persist. AI-tracked non-disclosure agreement (NDA) activity—a reliable leading indicator for pipeline volume—points to flat exit activity through the second half of the year.

Compounding this stagnant deal flow is a growing behavioral standoff between General Partners (GPs) and their investors. The report highlights a recent Institutional Limited Partners Association (ILPA) poll revealing that limited partners begin losing confidence in a sponsor if a full exit closes at a discount of more than 5% to its prior carrying value. Faced with this reputational risk, GPs are heavily incentivized to hold onto assets rather than selling into a tough market at a markdown. Instead of realizing returns, they are choosing to wait and force portfolio companies to eventually "grow" into their elevated valuations. This dynamic is a primary driver behind the broader aging of private equity portfolios, leaving investors to navigate a highly mature, illiquid market where distributions remain difficult to come by.

Economic Calendar: Week Ahead (Eastern Time)

Tues, 6/23 @ 9:45 am: U.S. Flash Manufacturing PMI

@ 9:45 am: U.S. Flash Services PMI

Wed, 6/24 @ 10:00 am: New Home Sales

@ 4:00 pm: Federal Reserve Board releases annual bank stress test results

Thur, 6/25 @ 8:30 am: Durable Goods

@ 8:30 am: 3rd estimate GDP

@ 8:30 am: Weekly Jobless Claims

@ 8:30 am: Personal Income, M/M%

@ 8:30 am: Consumer Spending, M/M%

@ 8:30 am: PCE Price Index, M/M%, Y/Y%

@ 8:30 am: PCE Core Price Index, M/M%, Y/Y%

@ 11:00 am: Kansas City Fed Survey

Fri, 6/26 @ 8:30 am: Advance Economic Indicators Report

@ 8:30 am: Wholesale Inventories

@ 8:30 am: Retail Inventories

@ 10:00 am: U. Michigan Final Consumer Survey

The Team Behind Friday Focus

Mary Ahn

Investment Research and Portfolio Strategy Manager

Cal Jones, CFA

Managing Director of Fixed Income

Eric Speron, CFA

Managing Director of Equities

Alton Tjahyono, CFA

Sr. Investment Strategist