7 minute read

Smart insight and clear visuals that matter – what we’re watching now and how intention and conviction shape our portfolios.

Markets

History has often shown that the stock market has a specific breaking point when it comes to energy costs. When the price of U.S. crude oil jumps 35% to 50% above its two-year average, stock returns typically turn negative. Currently, that "danger zone" sits between $93 and $97 per barrel.

Why This Matters:

- The "Affordability" Pressure Point - Iran is may be using economic hardship as a weapon, betting that "affordability" issues will force the U.S. to retreat.

- Lofty Valuations- This price spike is a major threat today because stock prices are already at their highest levels since the "Y2K" tech bubble of 2000. This leaves very little room for error.

- The Safe Haven Failure- Usually, investors buy bonds when stocks get shaky. However, because governments are being forced to spend more on defense and energy, bonds are no longer acting as "Safe Havens".

- The "Sell Everything" Risk- As long as oil stays elevated and the "fog of war" remains thick, the risk that investors will simply "sell everything" remains high.

Budget

2027 Budget

The Trump administration released its proposal for the 2027 budget on April 3rd. The new 2027 budget proposal signals a massive shift toward military readiness, requesting $1.45 trillion for defense, a nearly 50% increase from two years ago. This surge reflects a world where nations are being forced to ramp up defense spending due to ongoing conflicts.

- The Funding Strategy: $350bn of the budget is targeted to come from reconciliation funding, which can avoid the 60-vote threshold in the Senate. Non-defense funding is set at $660bn, which is a 10% cut and hits every non-defense agency except NASA.

- The Deficit: The plan projects a $2.2 trillion deficit, assuming the U.S. economy grows quickly and brings in significant revenue from trade tariffs.

- The Political Risk: If the budget isn't approved before the November elections and the balance of power in Congress shifts, the administration will lose its primary shortcut to securing these funds.

Source: DoD

Credit

The All-clear Sign is Not Being Issued in Credit Markets

Yields have remained elevated on the move up in energy but is no longer believed to be the stock market’s concern as the market is within 2% of its all-time high. This chart from Doubleline is something to watch regarding inflation expectations.

If inflation rates stay elevated as demand weakens and as the higher cost of energy works its way through the system, one of our investors Bruce Richard's from Marathon makes a compelling case that credit should have its hands full still. Why?

- JPMorgan's latest tally of stressed and distressed credit in U.S. markets exceeds $200B across High Yield and Syndicated Loans NOT INCLUDING private credit. Marathon thinks stressed private credit is another $200B and $100B at risk on direct lending. When you add the at-risk portion of Direct Lending to the equation, we are looking at ~$500B+ requiring some form of capital solution in the years ahead.

-

The Morningstar LSTA Leveraged Loan Index has fallen from 98.0 to 94.5 as the distressed ratio of syndicated loans is 8% and rising. Approximately 12% of private credit borrowers are now generating negative cash flow, with 25% operating with interest coverage below 1.0x. You have seen me normalize equities for stock based, compensation, GAAP earnings and depreciation but applying the same idea to credit is interesting. Richards says that this statistic rises to ~33% when using actual EBITDA, rather than pro-forma adjusted EBITDA which on average has been adjusted higher by 20%. (See adjustment graph below.)

Source: Marathon

With the exception of the energy sector, which is performing exceptionally well for obvious reasons, all other 20 industry sectors have issues brewing as JP Morgan shows below.

Private Credit

US crude exports are projected to hit a record high in April as consumers in Asia hunt for supplies to replace Middle Eastern oil lost because of the Iran war.

-

Oil research group Kpler estimates exports will jump by almost a third to 5.2mn barrels per day this month, up from 3.9mn b/d in March.

-

Demand from consumers in Asia will rise by 82% to 2.5mn b/d.

Tech

There’s been a lot of AI job market doomerism recently, especially about the prospects for aspiring white-collar professionals just out of school.

-

The unemployment rate for recent college graduates in the US, at 5.6%, is well above the pre-pandemic lows and is higher than the overall rate of 4.2%.

-

The unemployment rate for recent graduates has ticked up since 2023 but not seeing a divergence in the trend in the unemployment rate between the fresh college graduates and non-graduate workers of the same age.

-

The trend in job openings in areas likely to be disrupted by AI, such as legal and accounting services, haven’t diverged much from the wider market.

Capabilities and Adoption

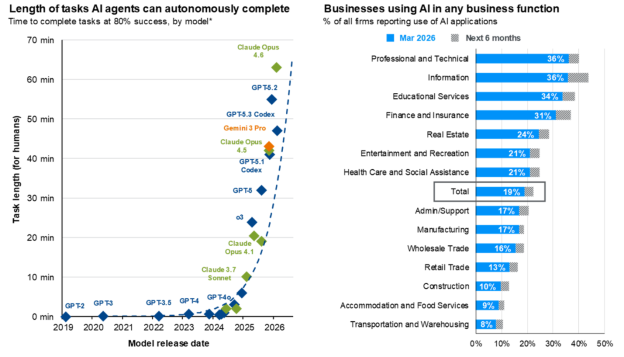

The chart on the left shows the duration of tasks that AI agents can complete autonomously with an 80% success rate, highlighting that this capability has been doubling roughly every seven months. The right shows AI adoption rates across U.S. firms. As AI capabilities continue to improve, adoption rates should rise, translating into notable productivity gains over time.

Source: J.P. Morgan Asset Management; (Left) METR, “Measuring AI Ability to complete long tasks”; (Right) Census Business Trends and Outlook Survey.. – as of March 31, 2026

REITs

When comparing the cap rates of publics REITs vs. private real estate, there continues to be a valuation gap to legacy real estate assets. This continues to help explain why there have been many acquisitions of public REITs by private equity.

Economic Calendar: Week Ahead (Eastern Time)

Mon, 4/13 @ 10:00 am: Existing Home Sales

Tues, 4/14 @ 8:30 pm: Producer Price Index/ Core PPI/ PPI YoY

Wed, 4/15 @ 8:30 am: Import Price Index

@ 8:30 am: Empire State Manufacturing Survey

@ 10:00 am: Home Builder Confidence Index

@ 2:00 pm: Fed Beige Book

Thur, 4/16 @ 8:30 am: Initial Jobless Claims

@ 8:30 am: Philadelphia Fed Manufacturing Survey

Fri, 4/17 @ 8:30 am: Housing Starts

@ 8:30 am: Building Permits

The Team Behind Friday Focus

Mary Ahn

Investment Research and Portfolio Strategy Manager

Cal Jones, CFA

Managing Director of Fixed Income

Eric Speron, CFA

Managing Director of Equities

Alton Tjahyono, CFA

Sr. Investment Strategist