4 minute read

Smart insight and clear visuals that matter – what we’re watching now and how intention and conviction shape our portfolios.

Markets

Recap of 2025 Total Returns

The year demonstrated the strongest cross-asset performance since 2009, with stocks and bonds rising together, credit spreads tightening, and commodities advancing.

- Gold: +64%

- International Developed ex-US: +35%

- Emerging Markets: +33%

- Nasdaq 100: +21%

- S&P 500: +18%

- Small Caps: +13%

- Commodities: +8%

- US Bonds: +7%

- Cash: +4%

- REITs: +3%

- Bitcoin: -6%

Source: Bloomberg

Key Narratives that Drove 2025

Policy & Fed Dynamics: Tariff-driven volatility culminating in the “Liberation Day” sell-off, but ultimately not much impact as the administration proved its willingness to heed market signals. Inflation fears eased and were balanced against labor market softness; Fed cut rates three times, starting in September, driving Treasury outperformance vs. European rates. Housing disinflation and lower commodity prices should provide a backdrop supportive of further accommodation in the early part of 2026.

AI Mega Trend: Whether it’s a bubble or not remains to be seen but either way we do believe this is also the mega trend of our time and it is impacting our market in three key ways:

- Equity market performance and related wealth effects: The Magnificent 7 is up ~25% (Alphabet +65%, Nvidia +40%). Source: Bloomberg

- Productivity story: Ultimately above trend growth despite soft payrolls. AI impact on labor still appears limited but is a critical area to watch.

- Capital investment boom: AI-driven CapEx is approaching $500bn, fueling issuance and increasing net supply of debt. Continued strength in this area, or at least stability, will be necessary to see a constructive backdrop for ongoing overall market and economic strength in 2026. Sustained corrections are typically driven by policy and we don’t see policy interference on the horizon.

Private credit concerns: Several high-profile defaults, fraud headlines, and the underperformance of the BDC universe in both equities and credit has driven a lot of this focus. We also suspect a lot of the concerns are about opacity, both real and perceived. That isn’t necessarily negative, and in fact is a feature rather than a bug. How the market manages through this first cycle of non-bank private credit at real scale will be a dominant theme over the next several years, and that dynamic will create plenty of risks and opportunities for investors. That said, we do see systemic exposures as very manageable at least for now.

Market Valuation Update – Four Lenses

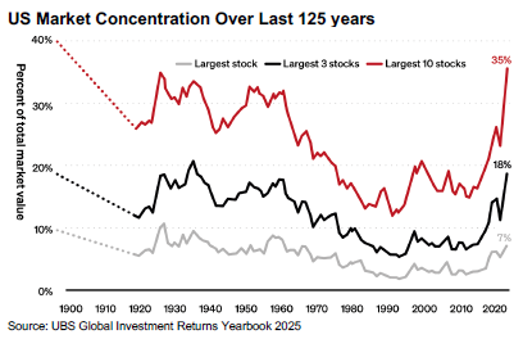

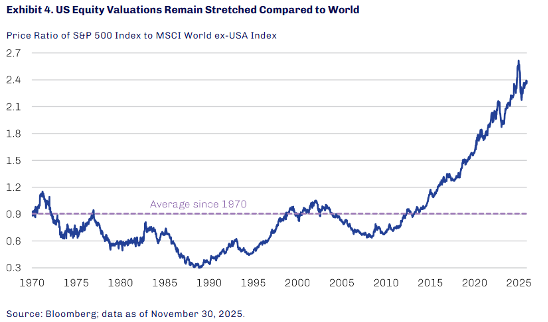

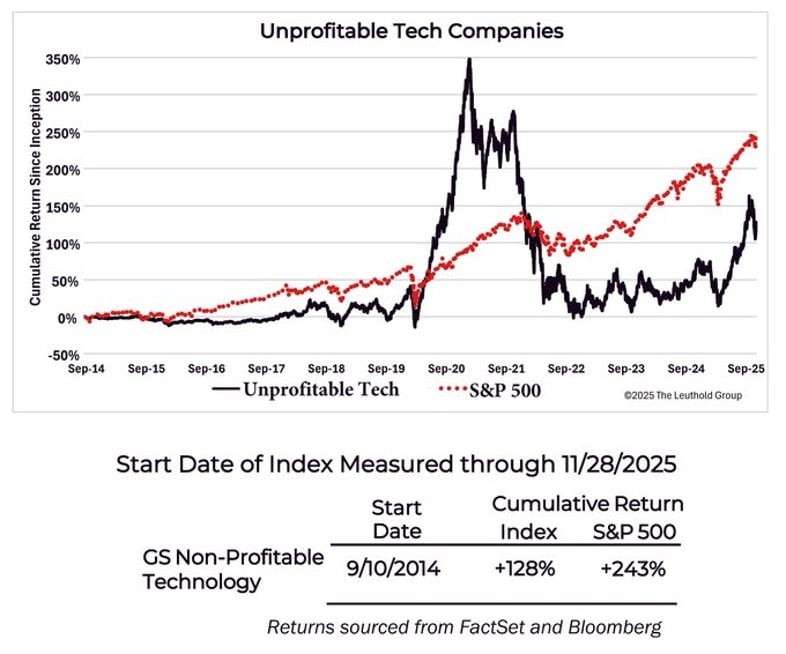

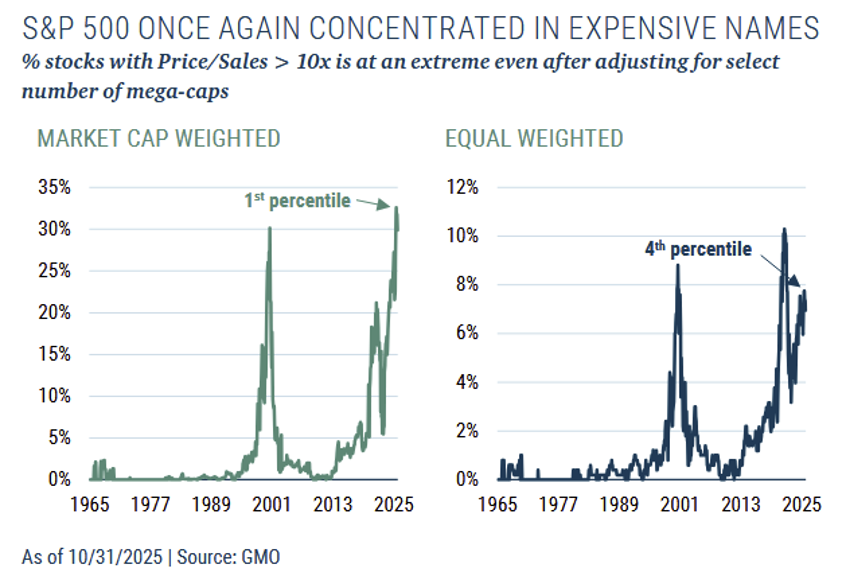

Not often do you get anything decades old, let alone centuries. Below is a chart of concentration in the US stock market since the McKinley presidency. Below that, the US versus International valuation for the past half century. Third, you can see how company profits weren’t the key to success in tech investment. The last chart shows we are in rare air regarding valuation whether it is market cap weighted or equally weighted.

Technology

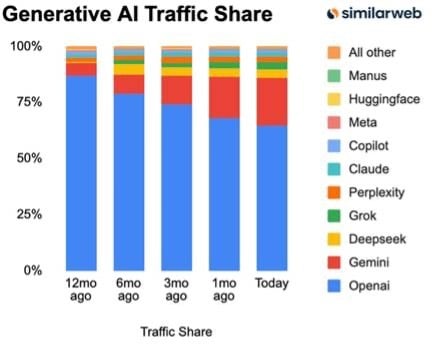

Google Gemini Market Share: Over the past 12 months, Gemini has emerged as a key player in generative AI, steadily increasing its traffic share and signaling growing market adoption.

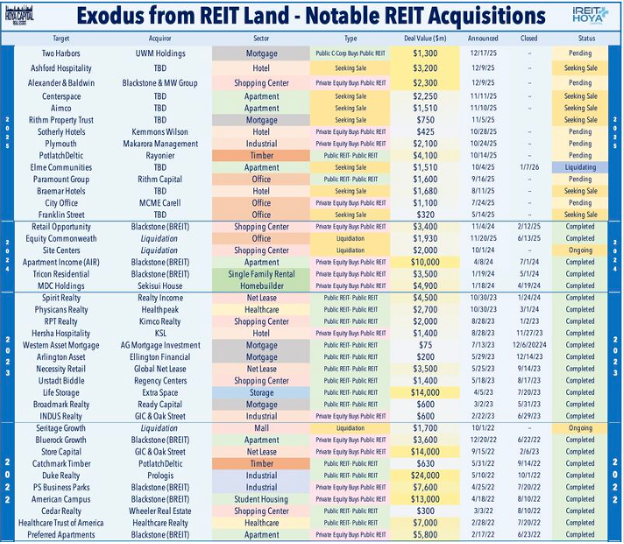

REITs

Public REITs are being sold, merged, and plan exits in masses in pursuit of maximizing shareholder value amid persistent valuation discounts applied to public REITs relative to their private market peers. 2025 saw more acquisitions than in the past three years and more than double the acquisitions than in 2024.

There is a significant difference when investing with managers on the public side vs. the private side. On the public side, investors pay a management fee to have their money managed. On the private side, investors are financing the business. Alignment of interest is always an important part of investing, but more attention is required when investing in private investments. General Partner (GP)s are incentivized to finance their deal (or fund) not only for low cost of debt, but also low cost of equity. GP percentage of the deal (or fund) matters. The lower the percentage of GP participation in financing, the more asymmetric the risk/return is for them. Among many things we review, skin in the game is a high priority.

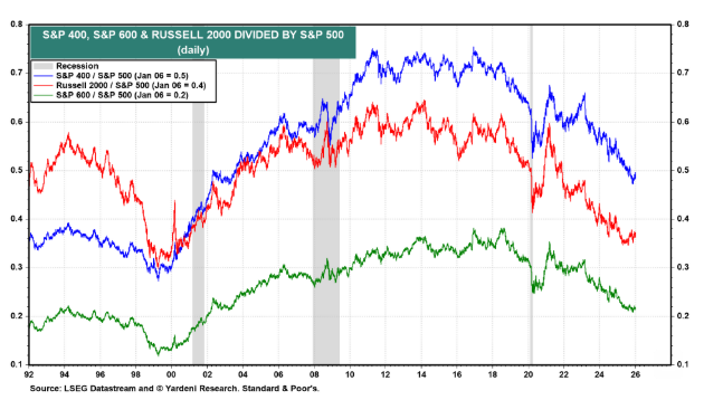

Small Cap

Will the S&P 400 Mid Caps and the S&P 600 Small Caps finally outperform the S&P 500 Large Caps this year? Small and Mid Caps have been underperforming the Large Caps since about 2018. They briefly outperformed in 2020 and 2021 following the Fed's dramatic easing of monetary policy in March 2020 in response to the pandemic. Smid Caps tend to underperform when investors fear a recession is coming, as in 2022 and 2023. But recession fears abated in 2024 and 2025, yet the Smid Caps continued to underwhelm. However, the earnings of both the S&P 400 and S&P 600 have been mostly flat since late 2022, while the forward earnings of the S&P 500 has soared to new record highs. It’s possible this is because Large Cap companies buy the most promising Smid Cap companies before their earnings really take off.

Economic Calendar: Week Ahead (Eastern Time)

Tues, 1/13

@ 830 am: U.S. Consumer Price Index

@ 10 am: U.S. New Home Sales

@ 2 pm: U.S. Budget Deficit

Wed, 1/14

@ 830 am: U.S. Retail Sales

@ 830 am: U.S. Producer Price Index

@ 10 am: Existing Home Sales

@ 2 pm: Federal Reserve’s Beige Book

Thurs, 1/15

@ 830am: Initial Jobless Claims

@ 830am: Philadelphia State Manufacturing Survey