7 minute read

Smart insight and clear visuals that matter – what we’re watching now and how intention and conviction shape our portfolios.

Tech

Hyperscalers: Negative Free Cash Flow

The first-quarter earnings of 2026 have made one thing abundantly clear: the world’s appetite for AI computing power is nowhere near satisfied. However, for the "hyperscalers"—the handful of tech giants building the backbone of this revolution—the cost of staying ahead is reaching eye-watering levels. While these investments are necessary to capture the future of Generative AI, they are beginning to weigh heavily on the present. For the first time in recent memory, the "forward free cash flow"—the actual cash left over after paying for these massive upgrades—is plummeting. For some of these giants, it is nearing negative territory.

Why does this matter? Historically, these companies have been cash machines, funding their growth out of their own pockets. If free cash flow turns negative across the board, something we’ve already seen with individual players like Oracle, it marks a significant shift in the investment narrative. When a company uses debt to build, investors naturally become much louder, demanding a faster and more concrete Return on Investment (ROI). The honeymoon period of "investing for the sake of the future" may soon give way to a "show me the money" era.

Despite earnings and free cash flow trending in opposite directions, strong data center revenue growth and expanding operating margins appear to be supporting investor confidence for now in the return on recent CapEx. That confidence may increasingly be tested as free cash flow comes under pressure.

Per Morningstar, AWS Q1 results were strong, with data center revenue growth accelerating to 28% year over year, and is now at a $150 billion annual run rate. Operating margin was 13.1% versus 11.8% a year ago.

Alphabet Q1 showed that Google Cloud sales accelerated sequentially and are up 63% annually. Morningstar estimates Gemini API sales are now generating around $15 billion in annual revenue, up from a $9 billion run rate last quarter. Operating margins expanded to 220 basis points, with cloud margins growing 15 points year over year to 33%.

A lurking concern continues to be the difference in accounting for revenue vs how depreciation is represented. Spending is recorded as immediate revenue and profit for suppliers like NVIDA and Broadcom, while the costs for the spenders are not yet fully recognized due to the lag in depreciation charges.

Source: Bloomberg, J.P. Morgan Asset Management.

Inflation and Rates

Trimmed Mean Inflation

According to Bloomberg, bond markets no longer expect the Fed to cut interest rates this year. Three of the Fed’s regional bank presidents voted against language that suggested the next rate move would be a cut. The critique by incoming Fed Chair Kevin Warsh suggests that the Fed’s current “mechanical” dependence on every incoming data point has created a cycle of inconsistent policy, arguing that this approach fosters inconsistency and market whiplash. Warsh is thus likely to prioritize a more filtered, long-term perspective on price stability. One such shift that has been circling would be in how the Fed defines "target" inflation. While the FOMC currently anchors itself to Core PCE, Warsh favors “Trimmed Mean inflation.” By discarding the "noise" of extreme outliers on both ends of the spectrum, this metric provides a smoother signal of underlying trends.

Interestingly, Trimmed Mean readings currently suggest that the economy is closer to the 2% goal than headline data implies—a nuance that could provide the cover for a more accommodative path once the "noise" subsides. Time will tell if TMI repeats the “transitory” blunder of Powell—trading a statistical filter for the lived reality of high prices.

Energy

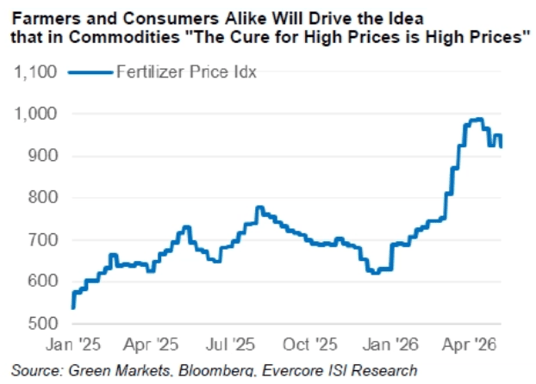

Despite elevated oil prices, the U.S. energy complex hasn’t meaningfully increased drilling activity as Richard Bernstein pointed out this week, we have seen no reactive increase in drilling activity to expand capacity and negate price increases. The C-Suite of U.S. energy companies are looking at the forward curve which shows the oil price fading late this summer, if it doesn’t, we will need rig activity to inflect up.

Source: Bloomberg

This dynamic also highlights an important distinction between operating companies and asset owners within the energy sector. Horizon Kinetics illustrates the vast difference between owning a corporation that drills for oil, and owning the cash flow directly connected to the price and production volume of oil.

While ExxonMobil is a hedge against inflation in theory, in practice, any meaningful inflationary trend is likely to be accompanied by higher interest rates. Higher rates reduce the value of most capital assets. The company’s reserves replacement costs will increase, perhaps substantially - everything from labor and equipment to new land leases and reserves.

Although net royalty acres are fixed at inception, advances in petroleum geology engineering mean that as of 2024, SBR’s proved oil and gas reserves are substantially higher than in 1999, despite all the production from those reserves over the course of those 25 years, and despite Sabine Royalty incurring no capital expenditures for 25 years.

Source: Horizon Kinetics

Source: Horizon Kinetics

Real Estate

Within public REITs we are seeing an inflection in earnings growth from its recent trough from 2% to 9%, much of it driven by the multi-year decline in construction growth. However, stagflation risk has emerged which generally is a headwind for REITs.

Source: Cohen & Steers

Equities

Howard Marks has pointed out that when buying the S&P 500 at a 23x P/E ratio, your 10-yr annualized return falls typically between +2% and –2%. Therefore garnering returns today could be stealing potential returns from tomorrow.

Source: DC Economics

While we’ve recently emphasized increased diversification, the chart below is a helpful reminder that despite improving growth across the Atlantic, it isn’t runaway growth by any means.

Economic Calendar: Week Ahead (Eastern Time)

Tues, 5/19 @ 10:00 AM: Pending Home Sales

Wed, 5/20 @ 2:00 PM: Fed’s May FOMC Meeting Minutes

Thur, 5/13 @ 8:30 AM: Initial Jobless Claims

@ 8:30 AM: Housing Starts

@ 8:30 AM: Building Permits

@ 8:30 AM: Philadelphia Fed Manufacturing Survey

Fri, 5/22 @ 10:00 AM: Consumer Sentiment

@ 10:00 AM: U.S. Leading Economic Indicators

The Team Behind Friday Focus

Mary Ahn

Investment Research and Portfolio Strategy Manager

Cal Jones, CFA

Managing Director of Fixed Income

Eric Speron, CFA

Managing Director of Equities

Alton Tjahyono, CFA

Sr. Investment Strategist